How to Buy a Home With No Down Payment and No Closing Costs Using a USDA Loan

Buying a home without a down payment is already a big win—but what if you could also eliminate your closing costs and walk into a home with almost zero out-of-pocket expenses? That’s exactly what’s possible with a USDA loan when you combine it with the smart use of seller concessions—especially when you find a home that’s already had a price reduction. Let’s break it down and show you exactly how it works.

✅ Step 1: Use a USDA Loan—$0 Down Payment

USDA loans are designed for rural and some suburban areas and offer:

- No down payment required

- Low interest rates

- Reduced mortgage insurance costs

You must meet certain income limits and purchase in a USDA-eligible area, but if you qualify, USDA loans are one of the most affordable ways to become a homeowner.

✅ Step 2: Use Seller Concessions to Cover Closing Costs

With a USDA loan, sellers can contribute up to 6% of the purchase price toward your closing costs and prepaid expenses. This includes:

- Title and escrow fees

- Lender fees

- Insurance and property taxes

- Even buying down your interest rate

That’s where strategy comes in—especially if the home you’re eyeing has recently had a price drop.

💡 Example Scenario: Making It a True No Money Down Deal

Let’s say you’re looking at a home that was originally listed at $300,000, but it’s been reduced to $285,000 after sitting on the market for a few weeks.

Rather than offering $285,000 and covering closing costs out of pocket, you do this:

🔹 Offer $300,000 (the original asking price)

🔹 Ask the seller for 6% in concessions—which is $18,000

🔹 Those concessions are used to pay all your closing costs and even potentially buy down your interest rate

👉 As long as the home appraises for $300,000, it’s a win-win.

The seller nets close to their reduced price after concessions, and you buy the home with no down payment, no closing costs, and possibly even a lower monthly payment thanks to a rate buy-down.

🚨 Why the Appraisal Matters

It’s critical that the home appraises for the full $300,000 offer price. If it doesn’t, the lender can’t approve the loan for that amount, and you may need to renegotiate.

That’s why this strategy works best when:

- The price reduction was made to attract buyers

- The original list price wasn’t overpriced

- The home is in good condition and supports the appraised value

Work with a knowledgeable real estate agent and loan officer to help ensure you're not overpaying for the property.

🏡 The End Result: A True $0-Out-of-Pocket Home Purchase

With the right home, the right loan, and the right offer strategy, you could:

- Buy a home with $0 down

- Have all closing costs covered

- Start building equity from day one

It’s a smart move—especially for first-time buyers looking to stretch their savings and get into a home without a large upfront investment.

Ready to Make It Happen?

If you’re interested in seeing what homes might qualify and how seller concessions can work in your favor, reach out today. I can show you how to structure a true no down payment purchase that helps you take full advantage of the USDA loan program.

Automatic Disqualifiers for USDA Mortgage Qualification

1. Credit History Disqualifiers

- More than one 30-day late payment on any credit account in the past 12 months

- Any 60-day or 90-day late payment in the past 12 months

- Foreclosure, short sale, or deed-in-lieu within the past 3 years

- Chapter 7 bankruptcy discharged less than 3 years ago

- Chapter 13 bankruptcy with less than 12 months of timely payments

- Federal debts currently delinquent or in default (e.g., student loans, tax liens)

- Judgments or unpaid child support unless resolved or in a verifiable payment plan with 3 months of on-time payments

- No established credit history and no non-traditional credit sources to support alternative credit

2. Income-Related Disqualifiers

- Total household income exceeds USDA limits for the county and household size (must include income of all household members, even if not on the loan)

- Unstable or unverifiable income (e.g., self-employed borrowers without 2 years of filed tax returns)

- Gaps in employment longer than 30 days in the past 2 years without a valid explanation or transition

- Bonus or overtime income not received for at least 12 consecutive months

3. Debt and DTI Ratios

- Monthly housing ratio (PITI) over 29% of gross monthly income without strong compensating factors

- Total debt ratio over 41% of gross monthly income without strong compensating factors

- Excessive revolving debt (e.g., maxed-out credit cards with no payment strategy or paydown plan)

4. Collections & Charge-Offs

- Non-medical collections exceeding $2,000 in total and not in a repayment plan or paid off

- Any open collection account related to housing or utility bills

- Any collection or charge-off within the last 12 months without explanation or resolution

- Judgments or liens not satisfied

- Any collection on federal debt (e.g., defaulted student loans or IRS debt)

5. Property & Occupancy

- Property not located in a USDA-eligible rural area

- Property not intended to be a primary residence

- Investment properties or second homes

- Non-compliant properties, including:

- Lack of access to utilities (water, electricity, sewage)

- Major structural issues or health/safety violations

- Incomplete construction (unless using USDA construction loan)

- Appraised value below purchase price with no cash to cover the difference

Potential Disqualifiers (Case-by-Case or Can Be Fixed)

Credit Factors

- Recent 30-day late payments (1 or less in 12 months) may be allowed with compensating factors

- Thin credit profile, but strong alternative credit (e.g., rental history, utility bills) may be considered

- Disputed accounts on credit may need to be removed or resolved

Income or Job Concerns

- New job within the last 6 months—can qualify if it's in the same field and stable

- Seasonal employment or variable income (e.g., tips, commission)—may qualify with two-year history

- Household member with income but no credit history—may impact eligibility if total income exceeds limits

Collections

- Medical collections, even if large, usually do not count against you

- Isolated charge-offs older than 12 months may be acceptable if no recent credit issues

Other Factors That Could Cause Denial or Delay

- Non-permanent residents or undocumented borrowers (must be U.S. citizens or qualified aliens)

- No valid social security number

- Inability to verify assets used for closing

- No reserve funds, when required as a compensating factor

- Misrepresentation on application (e.g., undisclosed debts, fake job history)

- Unverifiable gift funds for closing costs

Next Steps for Unqualified Borrowers

If someone is currently disqualified, they should be given clear direction on what to fix:

- Dispute or pay off negative credit items (especially recent collections)

- Establish on-time payments for at least 12 months

- Pay down revolving credit card balances below 30%

- Verify all income and employment documentation

- Explore credit repair or counseling services

- Plan to wait out seasoning periods for bankruptcies or foreclosures

- Adjust household income by excluding non-dependent cohabitants if possible

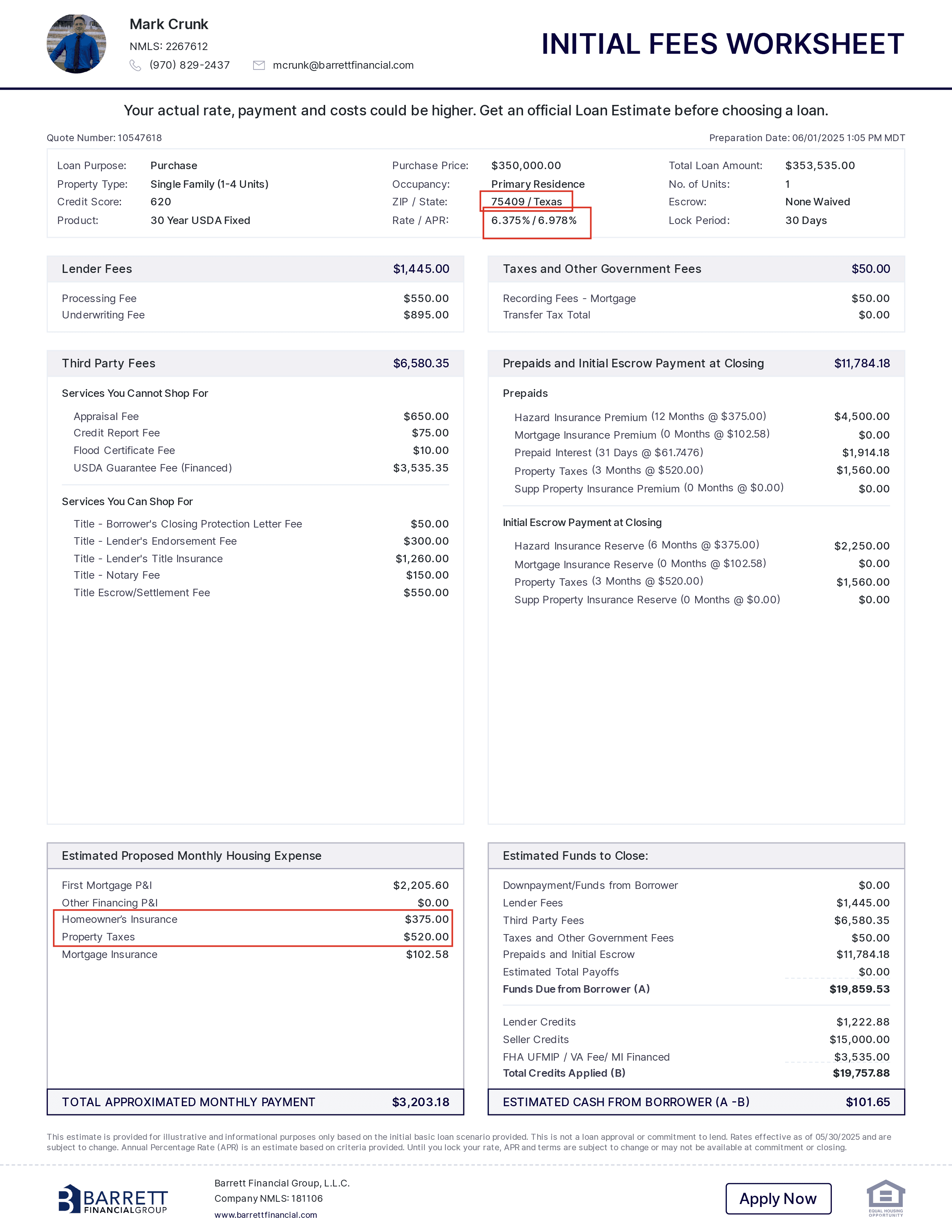

Here Is A Sample Hypothetical Loan Scenario Of A Home In An Eligible Area In Texas

Purchase a Home

Whether you're buying your first home or your dream home, we have a mortgage solution for you. Get your custom rate quote today.

Refinance your Home

We're committed to helping you refinance with the lowest rates and fees in the industry today. Getting started is quick and easy.

Apply Today

Our secure application is a few quick questions that takes about 7-10 minutes to complete and is required for a “Pre-Approval”. Get started today!