Recent Articles

Why So Many Self-Employed Business Owners Think They Can't Qualify for a Mortgage

If you're self-employed, own a small business, or work as an independent contractor, you've probably heard something like this: "Your tax returns don't show enough income to qualify." For many business owners, that's frustrating because your tax returns may not tell the whole story. The truth is, successful business owners often take legitimate deductions to reduce their taxable income. While those deductions can lower your tax bill, they can also make it harder to qualify for a traditional mortgage. That's where a bank statement loan may be worth exploring.

Published on 07/09/2026

Buying a Home Directly From the Seller? Read This First

Homebuying tips FSBO

Published on 06/22/2026

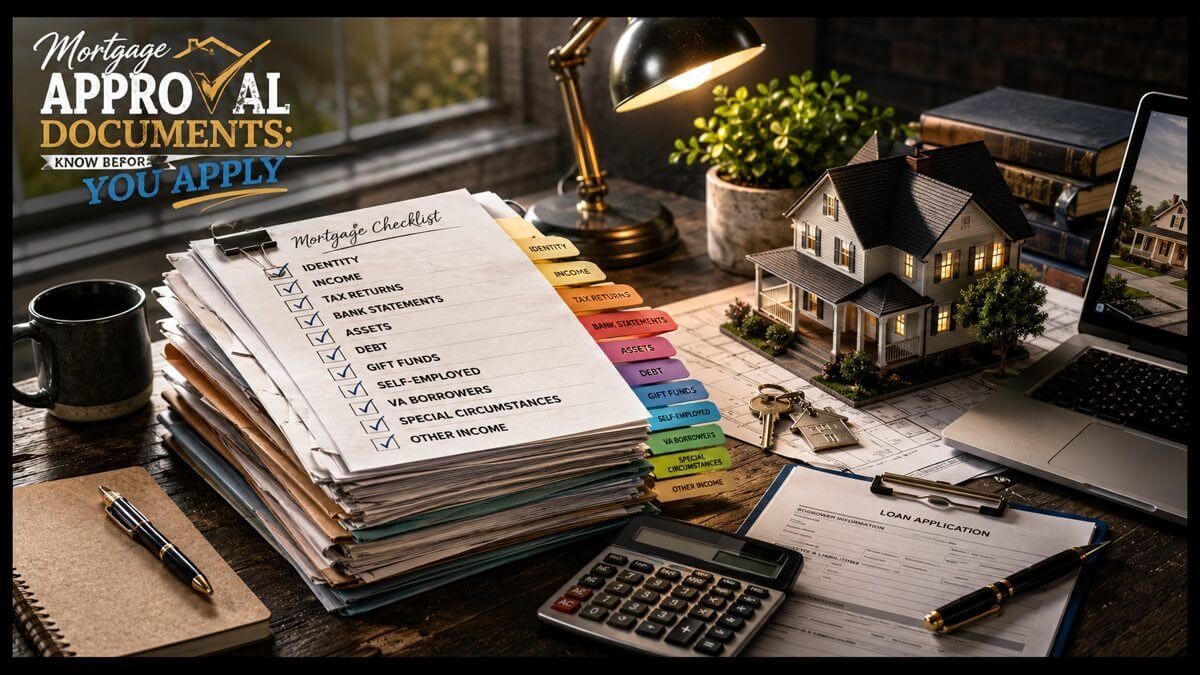

Mortgage Approval Documents: Know Before You Apply

Mortgage Approval checklist

Published on 06/11/2026

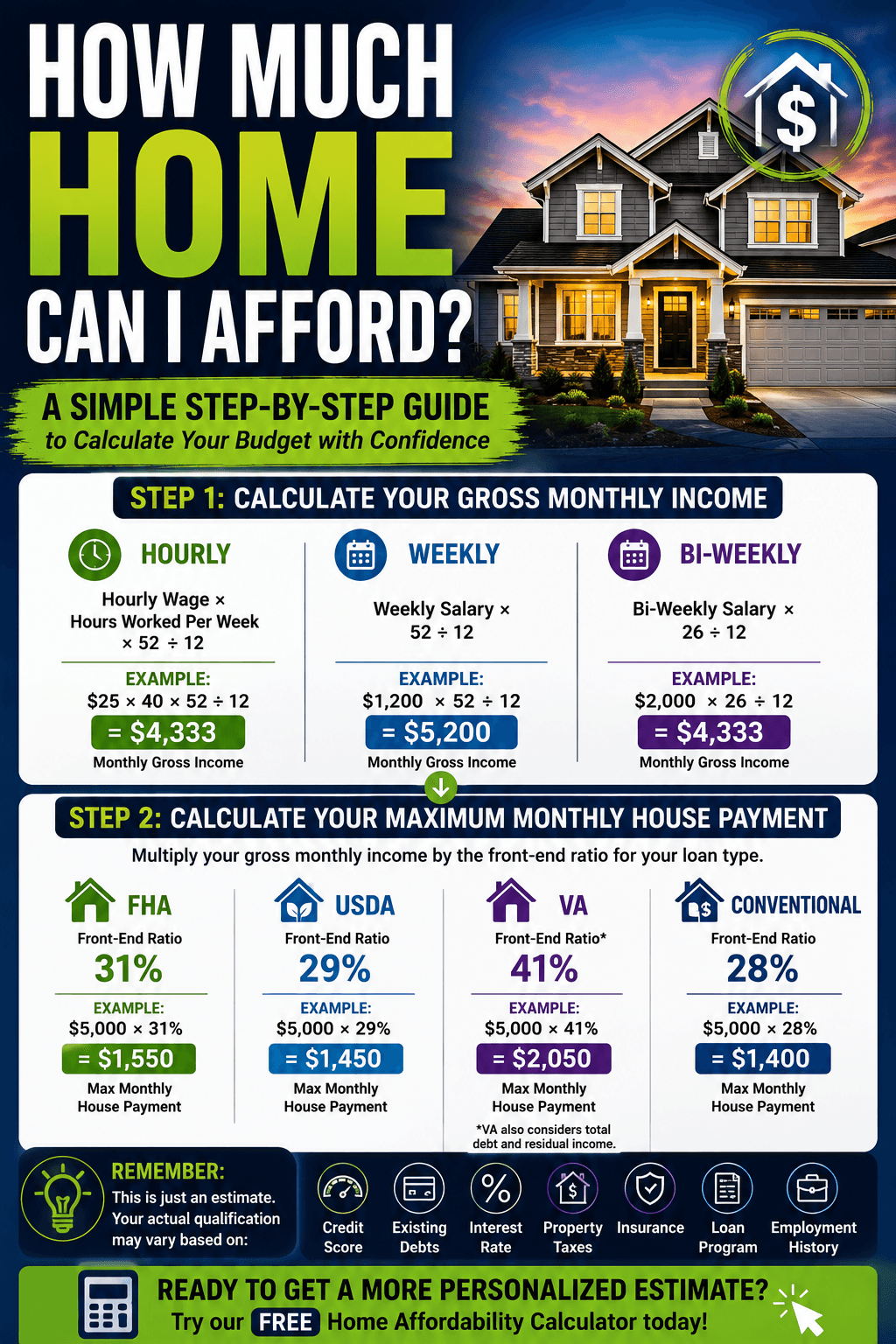

How Much Home Can I Afford? A Simple Step-by-Step Guide

One of the most common questions homebuyers ask is: "How much home can I afford?" Before you start looking at homes, it's helpful to understand how lenders estimate the maximum monthly housing payment that may fit your income. Let's break it down into a few simple steps.

Published on 06/01/2026

What If Rates Drop After You Lock?

What to do if rates drop after you locked your rate?

Published on 05/22/2026