USDA Mortgages: A Powerful No Down Payment Option—But Know What You’re Signing Up For

If you’ve been researching home loans and stumbled across the USDA mortgage program, you may have thought, “Wait — I can buy a house with no down payment, get a low interest rate, and maybe not even pay closing costs?” And yes — that’s the magic of the USDA loan. But before you start shopping for homes, there’s something equally important to understand: just because a loan is zero down doesn’t mean it’s zero stress on your monthly budget.

Let’s dig into the good — and the not-so-obvious — so you can make an informed decision.

✅ The Big Advantages of a USDA Mortgage

Zero Down Payment Required

USDA loans allow qualified buyers to finance 100% of the home’s purchase price. That’s a huge relief for those who haven’t been able to save a large down payment.Competitive Interest Rates

Because USDA loans are backed by the government, lenders often offer lower rates compared to conventional loans or even FHA loans.Seller-Paid Closing Costs

USDA guidelines allow the seller to pay up to 6% of the home’s price toward your closing costs. In some cases, buyers can get into a home with very little out-of-pocket expense.

⚠️ But Here's What You Need to Watch Out For

💸 Financing 100% at Today’s Rates Can Lead to Higher Payments

Even with a low interest rate, financing the full price of a home means you’ll have a larger loan balance, which equals a higher monthly payment — especially in the current rate environment where many mortgages are hovering in the 6–7% range.

🏡 Homeowners Insurance Can Be Expensive

In some areas — particularly those with risks of wildfires, hurricanes, or hail — insurance premiums have gone up significantly. This higher cost becomes part of your monthly mortgage payment and affects your debt-to-income (DTI) ratio, which is a major factor lenders use to determine if you qualify.

📈 Local Property Taxes Can Make or Break Your Budget

Taxes vary widely by city, county, and even neighborhood. In areas with higher property tax rates, monthly payments can be several hundred dollars more than in nearby towns. And yes — this affects your DTI ratio, too.

💡 What You Can Do to Protect Yourself

Get Insurance Quotes Early

Don’t wait until the last minute. Know what insurance will cost for the home you're interested in before you commit to it.Check Local Property Tax Rates

Property taxes can significantly impact your monthly payment. Look into the local rate and ask your lender to estimate your full monthly cost — not just principal and interest.Explore Homestead Exemptions

Some states, like Texas, offer homestead tax exemptions for primary residences that can reduce your annual property tax bill. It’s worth looking into if you plan to live in the home long-term.Consider Higher Insurance Deductibles

Choosing a higher deductible can help reduce your monthly insurance premium. Just make sure you have an emergency fund in case you ever need to file a claim.Know Your Debt-to-Income Limits

Financing 100% of the purchase price, along with higher insurance and taxes, might push your DTI above USDA loan limits — usually capped around 41% without compensating factors. This can make it harder to qualify.

🧠 Final Thought: Be Informed, Not Surprised

USDA loans are a fantastic tool to help people become homeowners with little to no upfront cost — but that doesn’t mean it’s always cheap month-to-month. Your interest rate, insurance premiums, and property taxes all come into play, and when you’re financing the full price of the home, every dollar counts.

Do your homework. Run the numbers. Ask questions. A great mortgage starts with great preparation — and knowing the full story helps you avoid sticker shock when that first payment is due.

Automatic Disqualifiers for USDA Mortgage Qualification

1. Credit History Disqualifiers

- More than one 30-day late payment on any credit account in the past 12 months

- Any 60-day or 90-day late payment in the past 12 months

- Foreclosure, short sale, or deed-in-lieu within the past 3 years

- Chapter 7 bankruptcy discharged less than 3 years ago

- Chapter 13 bankruptcy with less than 12 months of timely payments

- Federal debts currently delinquent or in default (e.g., student loans, tax liens)

- Judgments or unpaid child support unless resolved or in a verifiable payment plan with 3 months of on-time payments

- No established credit history and no non-traditional credit sources to support alternative credit

2. Income-Related Disqualifiers

- Total household income exceeds USDA limits for the county and household size (must include income of all household members, even if not on the loan)

- Unstable or unverifiable income (e.g., self-employed borrowers without 2 years of filed tax returns)

- Gaps in employment longer than 30 days in the past 2 years without a valid explanation or transition

- Bonus or overtime income not received for at least 12 consecutive months

3. Debt and DTI Ratios

- Monthly housing ratio (PITI) over 29% of gross monthly income without strong compensating factors

- Total debt ratio over 41% of gross monthly income without strong compensating factors

- Excessive revolving debt (e.g., maxed-out credit cards with no payment strategy or paydown plan)

4. Collections & Charge-Offs

- Non-medical collections exceeding $2,000 in total and not in a repayment plan or paid off

- Any open collection account related to housing or utility bills

- Any collection or charge-off within the last 12 months without explanation or resolution

- Judgments or liens not satisfied

- Any collection on federal debt (e.g., defaulted student loans or IRS debt)

5. Property & Occupancy

- Property not located in a USDA-eligible rural area

- Property not intended to be a primary residence

- Investment properties or second homes

- Non-compliant properties, including:

- Lack of access to utilities (water, electricity, sewage)

- Major structural issues or health/safety violations

- Incomplete construction (unless using USDA construction loan)

- Appraised value below purchase price with no cash to cover the difference

Potential Disqualifiers (Case-by-Case or Can Be Fixed)

Credit Factors

- Recent 30-day late payments (1 or less in 12 months) may be allowed with compensating factors

- Thin credit profile, but strong alternative credit (e.g., rental history, utility bills) may be considered

- Disputed accounts on credit may need to be removed or resolved

Income or Job Concerns

- New job within the last 6 months—can qualify if it's in the same field and stable

- Seasonal employment or variable income (e.g., tips, commission)—may qualify with two-year history

- Household member with income but no credit history—may impact eligibility if total income exceeds limits

Collections

- Medical collections, even if large, usually do not count against you

- Isolated charge-offs older than 12 months may be acceptable if no recent credit issues

Other Factors That Could Cause Denial or Delay

- Non-permanent residents or undocumented borrowers (must be U.S. citizens or qualified aliens)

- No valid social security number

- Inability to verify assets used for closing

- No reserve funds, when required as a compensating factor

- Misrepresentation on application (e.g., undisclosed debts, fake job history)

- Unverifiable gift funds for closing costs

Next Steps for Unqualified Borrowers

If someone is currently disqualified, they should be given clear direction on what to fix:

- Dispute or pay off negative credit items (especially recent collections)

- Establish on-time payments for at least 12 months

- Pay down revolving credit card balances below 30%

- Verify all income and employment documentation

- Explore credit repair or counseling services

- Plan to wait out seasoning periods for bankruptcies or foreclosures

- Adjust household income by excluding non-dependent cohabitants if possible

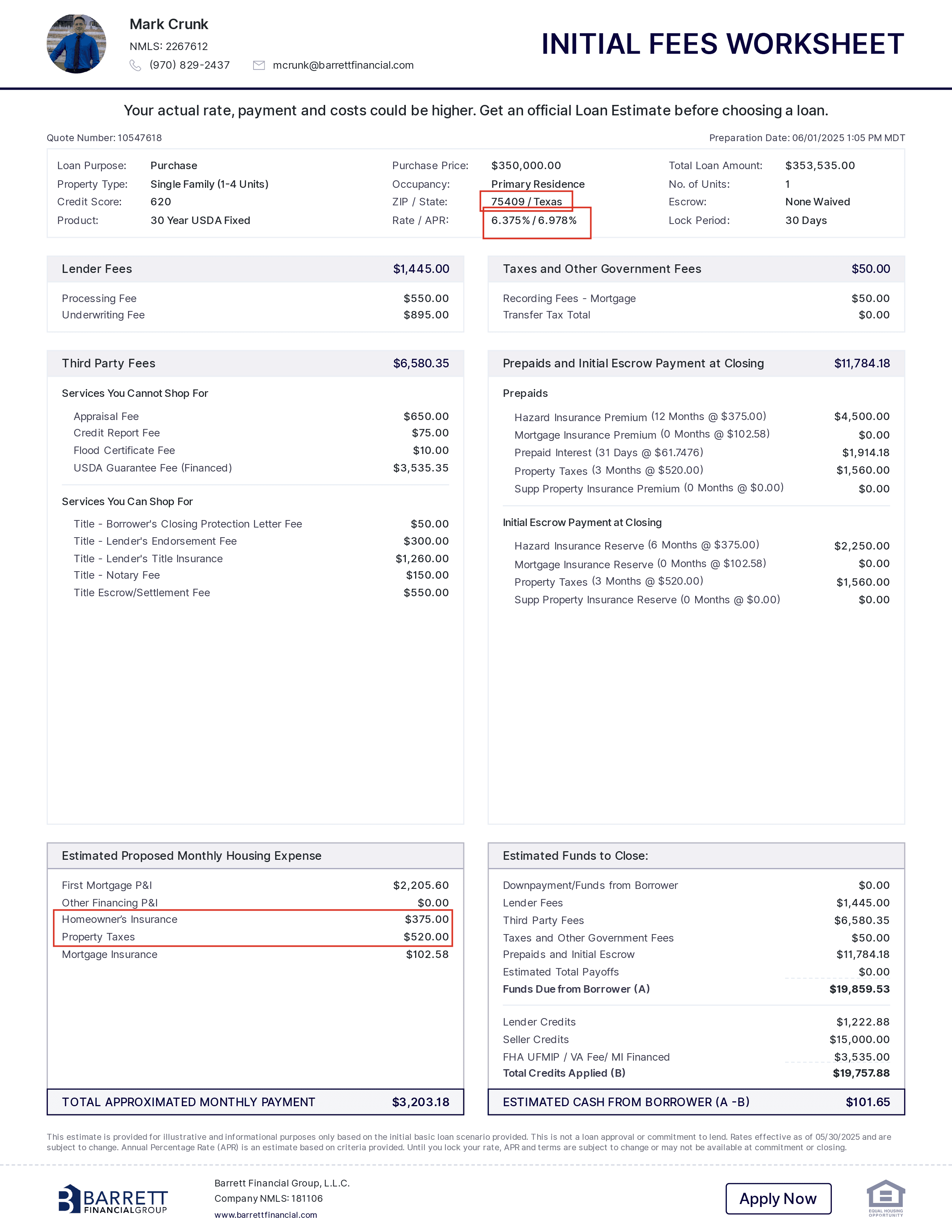

Here Is A Sample Of A Hypothetical Loan Scenario

Purchase a Home

Whether you're buying your first home or your dream home, we have a mortgage solution for you. Get your custom rate quote today.

Refinance your Home

We're committed to helping you refinance with the lowest rates and fees in the industry today. Getting started is quick and easy.

Apply Today

Our secure application is a few quick questions that takes about 7-10 minutes to complete and is required for a “Pre-Approval”. Get started today!