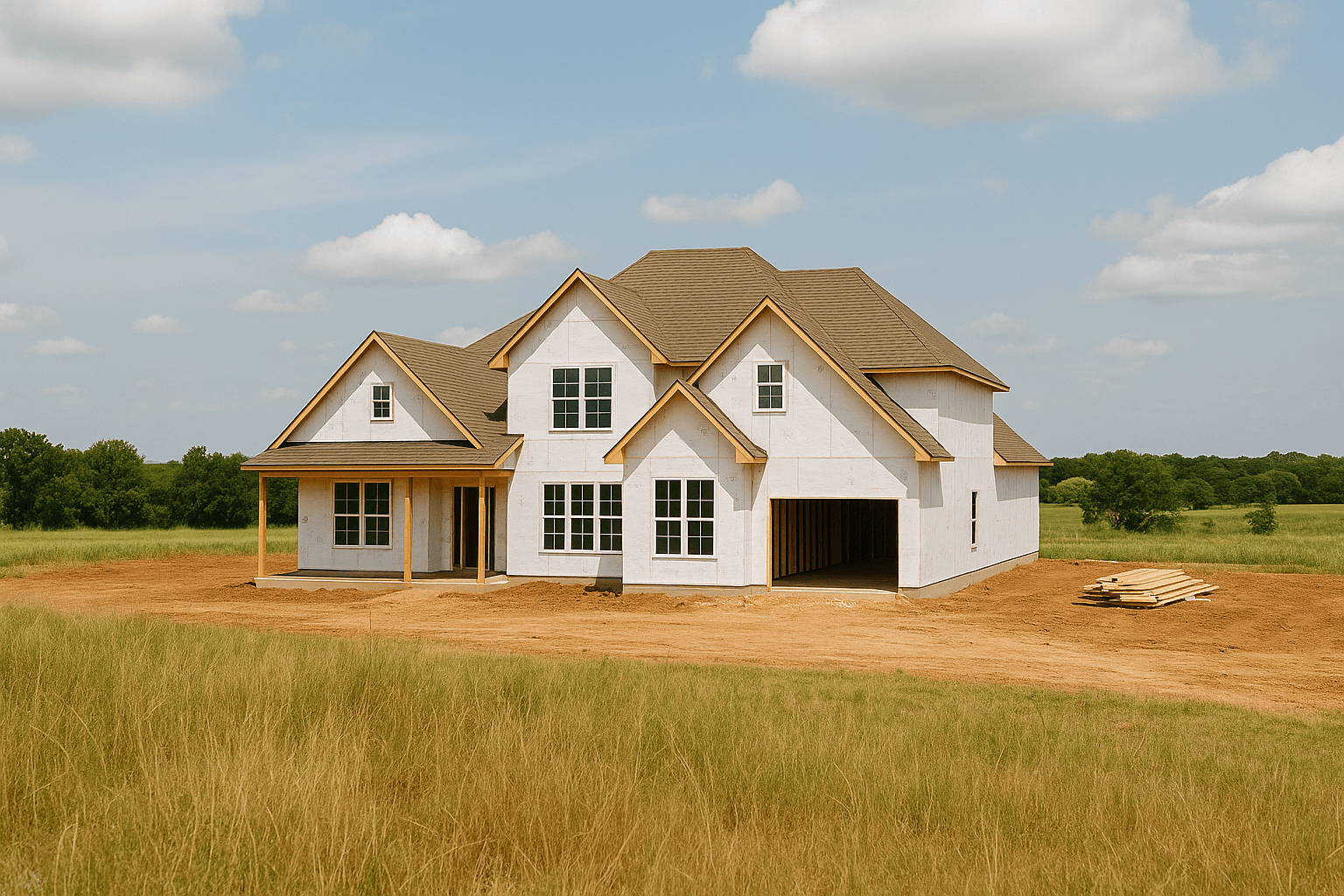

One Time Close Construction Loans

One-Time Close construction loans are the perfect solution for financing your dream home. These loans combine the construction, lot purchase, and permanent mortgage into a single closing, eliminating the need for multiple loans and saving you time and money.

We offer several options to suit your needs, including 0% down payment VA, 0% down payment USDA, 3.5% down payment FHA, and 3%, 5%, 10%, and 20% down payment Conventional One-Time Close loans:

- VA One-Time Close: Ideal for eligible veterans and active-duty service members, offering no down payment and competitive interest rates.

- USDA One-Time Close: Perfect for rural homebuyers, featuring zero down payment and favorable terms for eligible properties.

- FHA One-Time Close: A great choice for those with a smaller down payment, requiring as little as 3.5% and flexible credit requirements.

- Conventional One-Time Close: Designed for borrowers with strong credit, offering a range of down payment options and competitive rates.

If you already own land, you can use the equity as a down payment or to cover closing costs. Additionally, the equity can be applied to buy down your interest rate, making your loan more affordable.

With One-Time Close construction loans, you can build a manufactured home, modular home, or barndominium.

Let us help you make your dream home a reality!