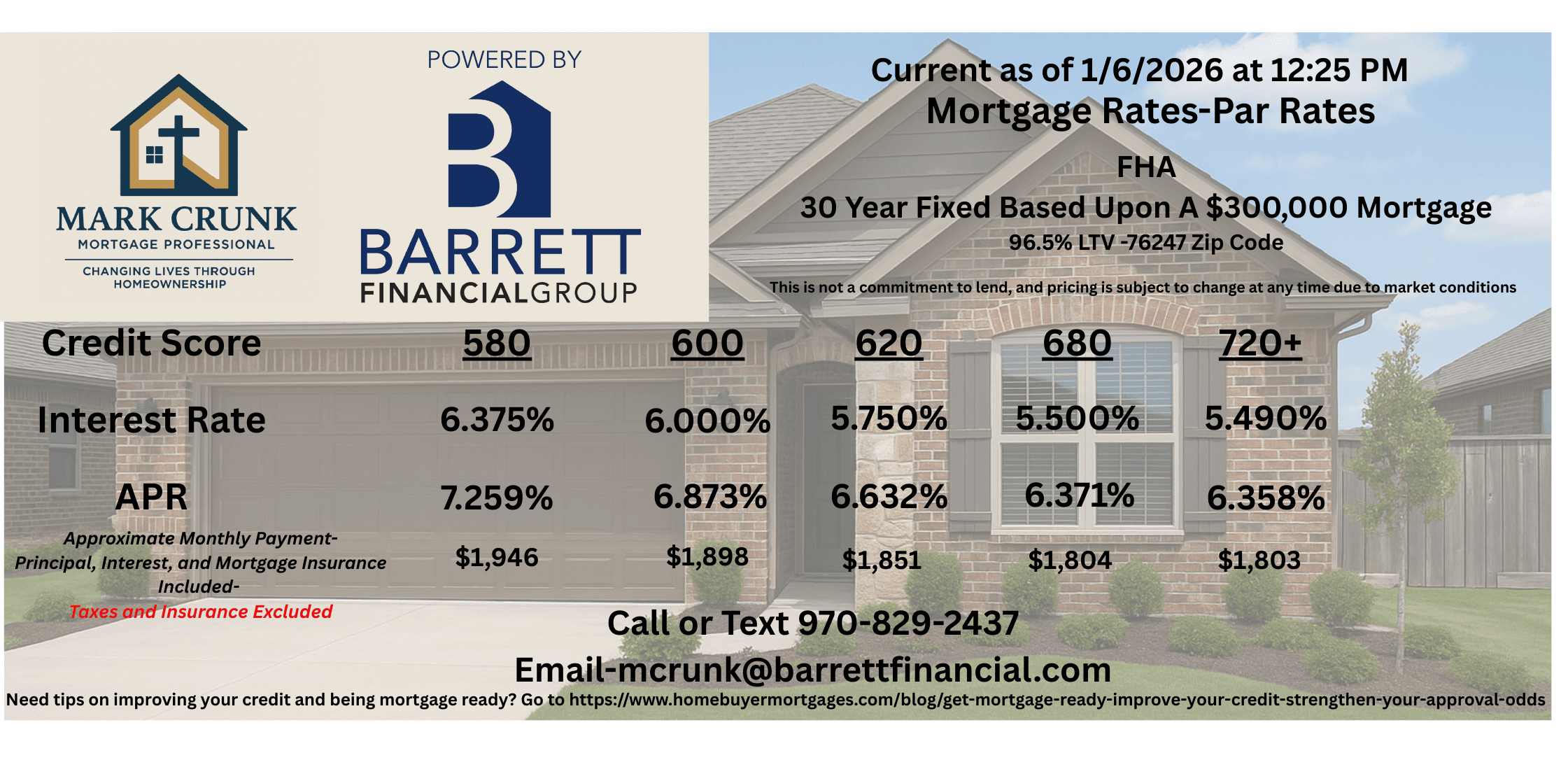

Dreaming of owning a home but worried about the down payment?

With the FHA $100 Down Payment Program, you could buy a HUD-owned home for as little as $100 down instead of the typical 3.5% down payment. Imagine moving into your own home with minimal upfront cost and starting to build equity sooner.

💡 What is the FHA $100 Down Payment Program?

When a home financed with an FHA loan goes into foreclosure, it often becomes a HUD-owned property. To encourage buyers to purchase these homes, HUD offers the $100 down payment incentive to make homeownership more attainable.

✅ Purchase a HUD-owned home using an FHA loan

✅ Pay only $100 down instead of thousands

✅ Available for owner-occupants only

✅ Must meet standard FHA guidelines and submit a full-price offer

✅ Who Qualifies for This Program?

You must meet FHA loan requirements, including:

✔️ Minimum credit score: 580 (some lenders require higher)

✔️ Debt-to-income ratio: Typically 43% or less

✔️ Employment: Stable, verifiable income with pay stubs, W-2s, or tax returns

✔️ Occupancy: Must live in the home as your primary residence

✔️ Valid SSN and ID: Required

✔️ Closing costs: Even with $100 down, you must cover closing costs and prepaid items (seller concessions can help)

❌ Automatic Disqualifiers

Unfortunately, not everyone qualifies. You may be disqualified if you:

- Are an investor (only owner-occupants qualify)

- Have credit scores below 580

- Have multiple late payments in the past 12 months, especially on rent or mortgage

- Have current accounts 90+ days late

- Are in bankruptcy without meeting waiting periods

- Had a foreclosure within the last 3 years (unless with extenuating circumstances)

- Have defaulted federal debt or student loans

- Cannot verify income or employment

- The property does not meet FHA safety and appraisal standards

🙌 Why Consider This Program?

✔️ Keep more money in your pocket for moving, furniture, or savings

✔️ Competitive FHA interest rates to keep payments manageable

✔️ Start building equity sooner, without years of down payment savings

👋 Ready to Find Out if You Qualify?

Imagine owning your own home with just $100 down. Let’s see if there’s a HUD home in your area that fits your needs and get you prequalified today.

You can check out current available properties at the HUD Homestore

📞 Questions? Let’s Talk.

Call or text: 970-829-2437

Email: mcrunk@barrettfinancial.com

NMLS#: 2267612

Disclosures

FHA $100 Down Payment Program is available for qualified buyers on HUD-owned properties only. Standard FHA guidelines apply. Closing costs and prepaid items still apply. Program availability and eligibility are subject to change without notice.

FHA $100 Down Payment Program FAQs

Q: Is this program really just $100 down?

A: Yes, for qualified HUD-owned homes using an FHA loan, the down payment is only $100 instead of the usual 3.5%. However, you still need to pay closing costs and prepaid items, unless those are covered by seller concessions.

Q: Who is eligible for this program?

A: Buyers who:

- Plan to live in the home as their primary residence

- Qualify for an FHA loan (minimum 580 credit score, stable income, acceptable debt ratios)

- Make a full-price offer on an eligible HUD-owned property

Q: What’s the catch?

A: There isn’t really a catch, but you must:

- Buy a HUD-owned home

- Meet FHA loan requirements

- Understand the home is sold as-is and must meet FHA safety standards

Q: Can investors use this program?

A:No, only owner-occupants (buyers planning to live in the home) are eligible.

Q: Are there automatic disqualifiers?

A: Yes. You won’t qualify if you:

- Have a credit score below 580

- Have multiple recent late payments, especially on rent/mortgage

- Have accounts 90+ days late

- Are currently in bankruptcy without meeting FHA waiting periods

- Had a foreclosure within the last 3 years (unless with an approved exception)

- Have defaulted federal debt or student loans

- Can’t verify income or employment

- Are buying as an investor

- The property does not meet FHA appraisal and safety standards

Q: What about closing costs?

A: Closing costs and prepaid items are still required. However, these can often be covered by seller concessions or negotiated credits to minimize out-of-pocket costs.

Q: Does the property need to be in perfect condition?

A: No, but it must meet FHA minimum property standards for safety and livability. Issues like structural damage, roof problems, or major hazards must be repaired before closing or financed through an FHA 203k renovation loan.

Q: How do I find HUD homes in my area?

A: You can search HUD’s official website (https://www.hudhomestore.gov) or contact me directly. I can provide you with a list of available HUD-owned homes that qualify for this program in your area.

Q: How fast can I close on a HUD home with this program?

A:Typical FHA timelines apply, often 30-45 days, depending on your lender, appraisal, and inspection processes.