Recent Articles

BIG NEWS: Mortgage Rates Are at Their Lowest Level in Years—What That Means for You

Find out what this rate drop means to you for buying a new home.

Published on 01/19/2026

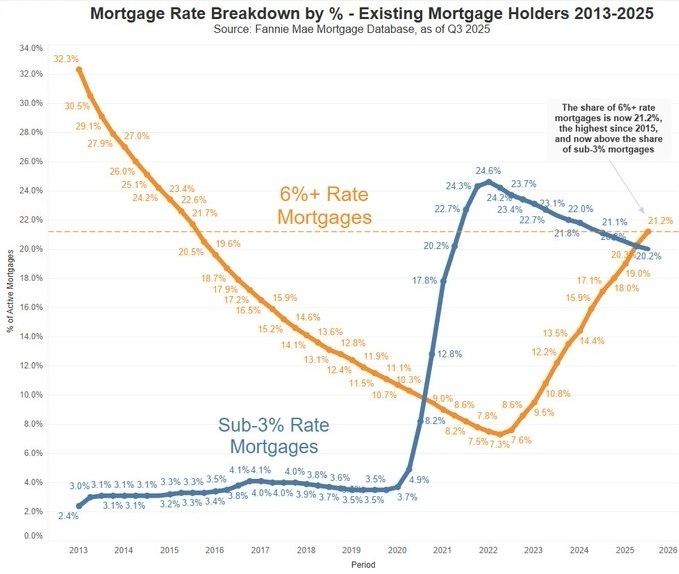

Lock-in Effect: Something big just happened in the U.S. Housing Market

Find out what the experts are anticipating for 2026 housing

Published on 01/12/2026

A Tale of Two Brothers: Renting vs. Buying Over 30 Years

What happens when two people do nearly everything right financially—but make one different housing decision? This simplified hypothetical explores how time, discipline, housing costs, and appreciation affect long-term net worth. The numbers are intentionally clean and conservative, but the lesson is anything but small.

Published on 01/07/2026

Holiday Week Catch-Up: Mortgage Rates Hover Near 2-Month Lows

A holiday-week catch-up: light trading kept markets mostly sideways, but the average 30-year fixed edged to near two-month lows as bonds got a small lift from Europe and pending home sales improved.

Published on 12/30/2025

The Hidden Costs That Can Make or Break Your Mortgage Approval

Why Taxes and Insurance Matter More Than You Think When most homebuyers start house hunting, they focus on one number: “How much home can I afford?” Usually, that number is based on the purchase price and estimated mortgage payment. But there are two often-overlooked line items that can quietly shrink your buying power—or even stop a deal in its tracks: 👉 Property taxes 👉 Homeowner’s insurance Let’s break down why these matter so much, how they affect your debt-to-income ratio (DTI), and what you can do to stay ahead of surprises.

Published on 12/29/2025

Inflation Cools in November — What It Means for Mortgage Rates

Inflation slowed in November after peaking earlier this fall. Here’s what that means for mortgage rates and what homebuyers should watch next.

Published on 12/18/2025

Fed Cuts Again, But Dot Plot Steers Mortgage Rate Outlook

The Fed cut rates by 0.25% and ended quantitative tightening, but the real story for the average 30-year fixed is in the dot plot and Powell’s comments. Here’s what that means for mortgage rates and homebuyers.

Published on 12/10/2025

This Week in Mortgage Rates: Buyers Are Back as Rates Hover in the Low 6s

Mortgage rates bounced around but stayed in a tight range near the low 6% area this week, while purchase applications hit their highest level since early 2023 and refinance demand more than doubled compared to last year. Here’s what that means if you’re thinking about buying or refinancing.

Published on 12/06/2025

Stronger Data Last Week Caused a Slight Rate Bump

Stronger jobless-claims and durable-goods data from last week pushed the average 30-year fixed slightly higher, but mortgage rates are still near recent lows. Here’s what that means for buyers and homeowners

Published on 12/01/2025