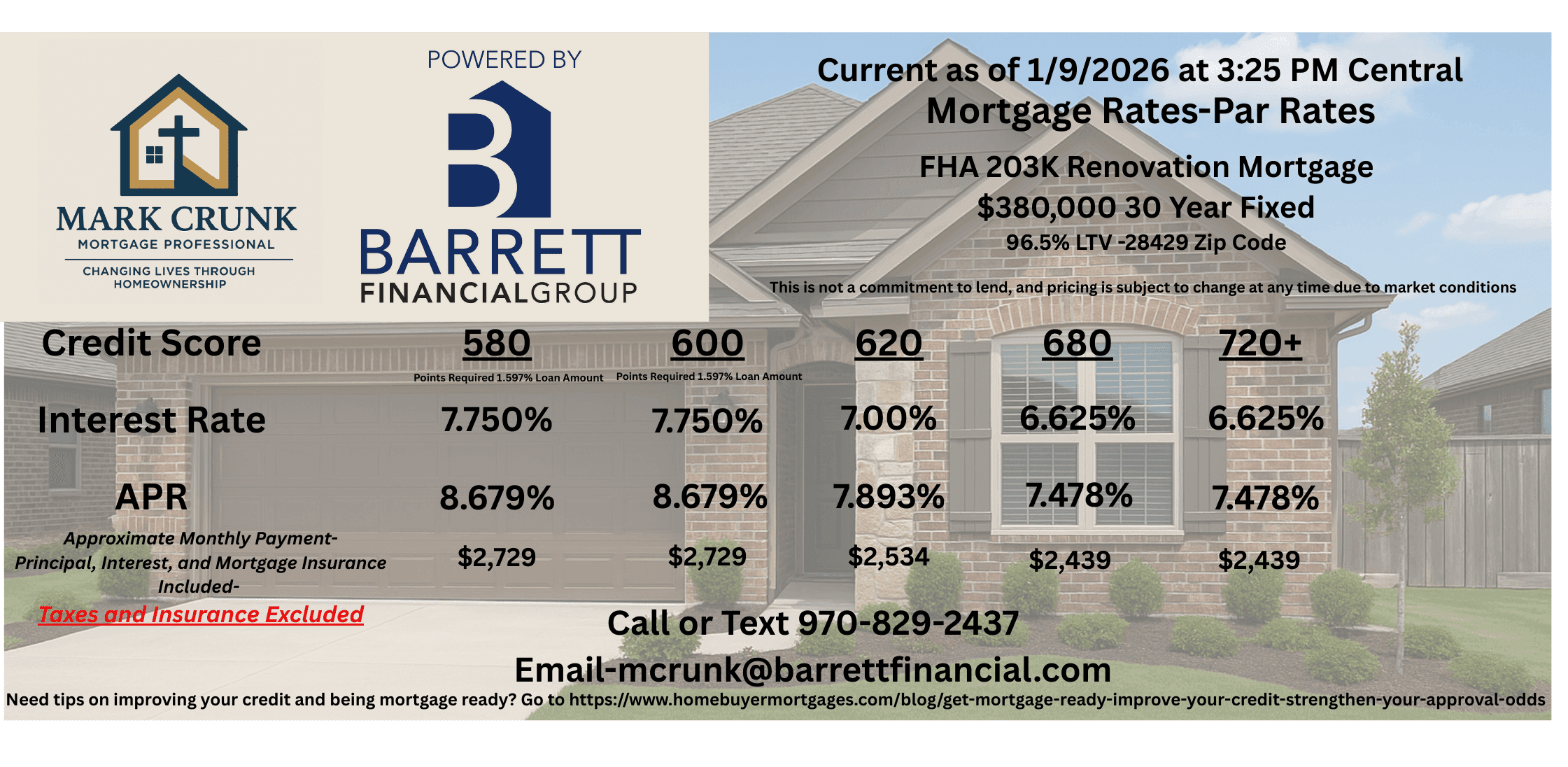

FHA 203(k) Renovation Mortgage

The above FHA 203k Home Renovation Mortgage Scenario hypothetical example is based upon a $100,000 purchase of an abandoned home with a $250,000 renovation budget and an approximate $45,000 reserve fund

Buy, Renovate, and Finance it all in one loan.

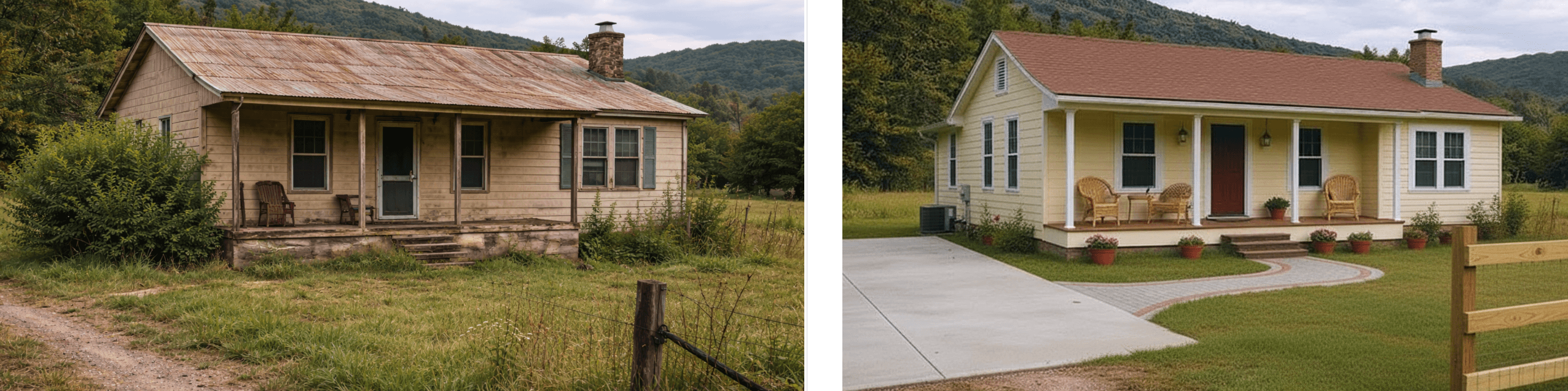

The FHA 203(k) renovation mortgage allows homebuyers and homeowners to purchase or refinance a property and finance renovations with a single mortgage. Instead of taking out separate loans for the purchase and repairs, the FHA 203(k) combines everything into one streamlined solution.

Backed by the Federal Housing Administration, this program is designed to help buyers transform homes that may not qualify for traditional financing due to condition issues.

What Is an FHA 203(k) Loan?

An FHA 203(k) loan is a government-insured mortgage that allows you to:

- Buy a home that needs repairs or updates

- Finance renovation costs into the loan

- Base the loan amount on the after-improved value of the property

This program is ideal for buyers who find a home they love but need to fix outdated features, safety issues, or cosmetic problems.

Two Types of FHA 203(k) Loans

1. Limited (Streamline) 203(k)

Best for smaller, non-structural repairs.

Key features:

- Renovation budget up to $75,000

- No structural changes allowed

- No consultant required (in most cases)

Eligible improvements include:

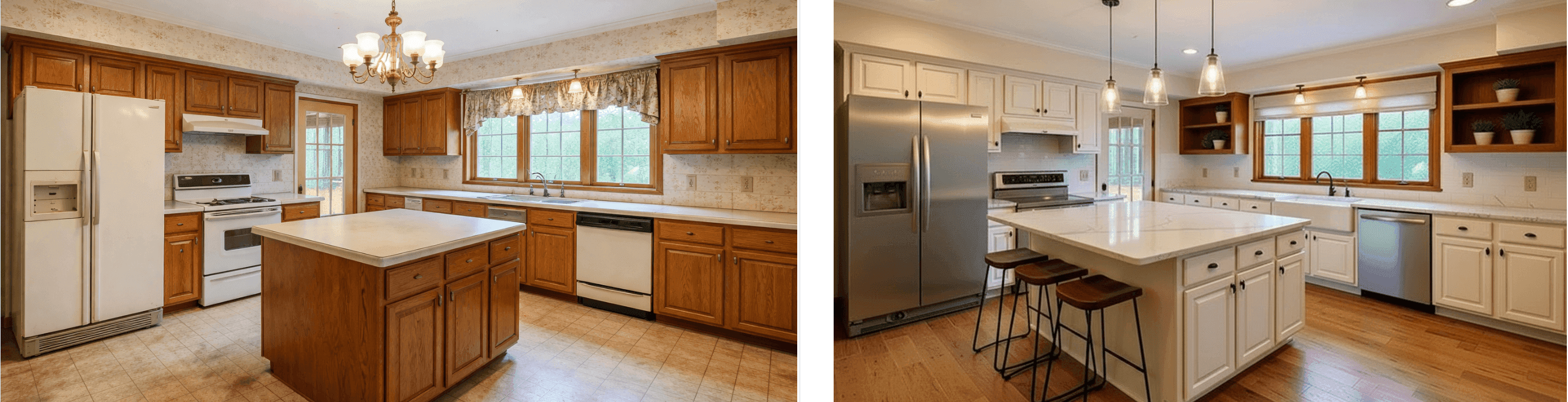

- Flooring, paint, drywall

- Kitchen or bathroom updates (no layout changes)

- Roof repair (not structural rebuild)

- HVAC replacement

- Appliances

- Minor electrical or plumbing repairs

2. Standard (Full) 203(k)

Designed for major renovations and structural repairs.

Key features:

- No set maximum renovation limit (based on loan limits)

- Structural changes allowed

- Usually Requires a HUD-approved 203(k) consultant

- Draw schedule during construction

Renovation funds can include up to six months of temporary housing while work is completed

Eligible improvements include:

- Structural repairs

- Room additions

- Foundation work

- Converting a single-family home from multi-unit

- Accessibility upgrades

- Kitchen and bathroom updates (non-structural)

- Roof replacement

- HVAC, plumbing, and electrical upgrades

- Flooring replacement

- Interior and exterior paint

- Appliance installation

- Window and door replacement

- Decks, patios, and porches

- Basement finishing (non-structural)

- Energy efficiency and weatherization upgrades

Minimum Requirements to Qualify

Credit Score

- 580+ for 3.5% down (most lenders)

- Lower scores may require higher down payment

Down Payment

- 3.5% minimum based on the total loan amount (purchase + renovations)

Employment & Income

- Stable employment history (typically 2 years)

- Verifiable income

- Must meet FHA debt-to-income (DTI) guidelines

Occupancy

- Primary residence only

- Not for investment or second homes

How Much Can You Borrow?

The FHA 203(k) loan amount is based on the lesser of:

- Purchase price + renovation costs, or

- Appraised value after improvements

All loans must stay within county FHA loan limits, which vary by location.

What Can the 203(k) Be Used For?

✔️ Outdated or damaged homes

✔️ Cosmetic upgrades that prevent traditional financing

✔️ Properties with safety or livability issues

✔️ Fixer-uppers listed below market value

✔️ Homes that won’t qualify for FHA, USDA, or Conventional “as-is”

Automatic Disqualifiers for FHA 203(k)

You may not qualify if:

- The property is not owner-occupied

- The home will be used as an investment or rental

- Renovations include luxury items (pools, outdoor kitchens, tennis courts)

- The property cannot be completed within required timelines

- Borrower income or credit cannot be documented

- Renovation plans exceed FHA guidelines

Benefits of an FHA 203(k) Loan

- One loan, one payment

- Finance repairs without high-interest credit cards or personal loans

- Increase home value immediately

- Compete with cash buyers on fixer-uppers

- Turn “unlivable” homes into long-term residences

Is an FHA 203(k) Right for You?

If you’re struggling to find a move-in-ready home, the FHA 203(k) could open doors to properties other buyers overlook—while allowing you to build equity through renovation.

📩 Want to see if a 203(k) works for your situation?

Call or Text 970-829-2437