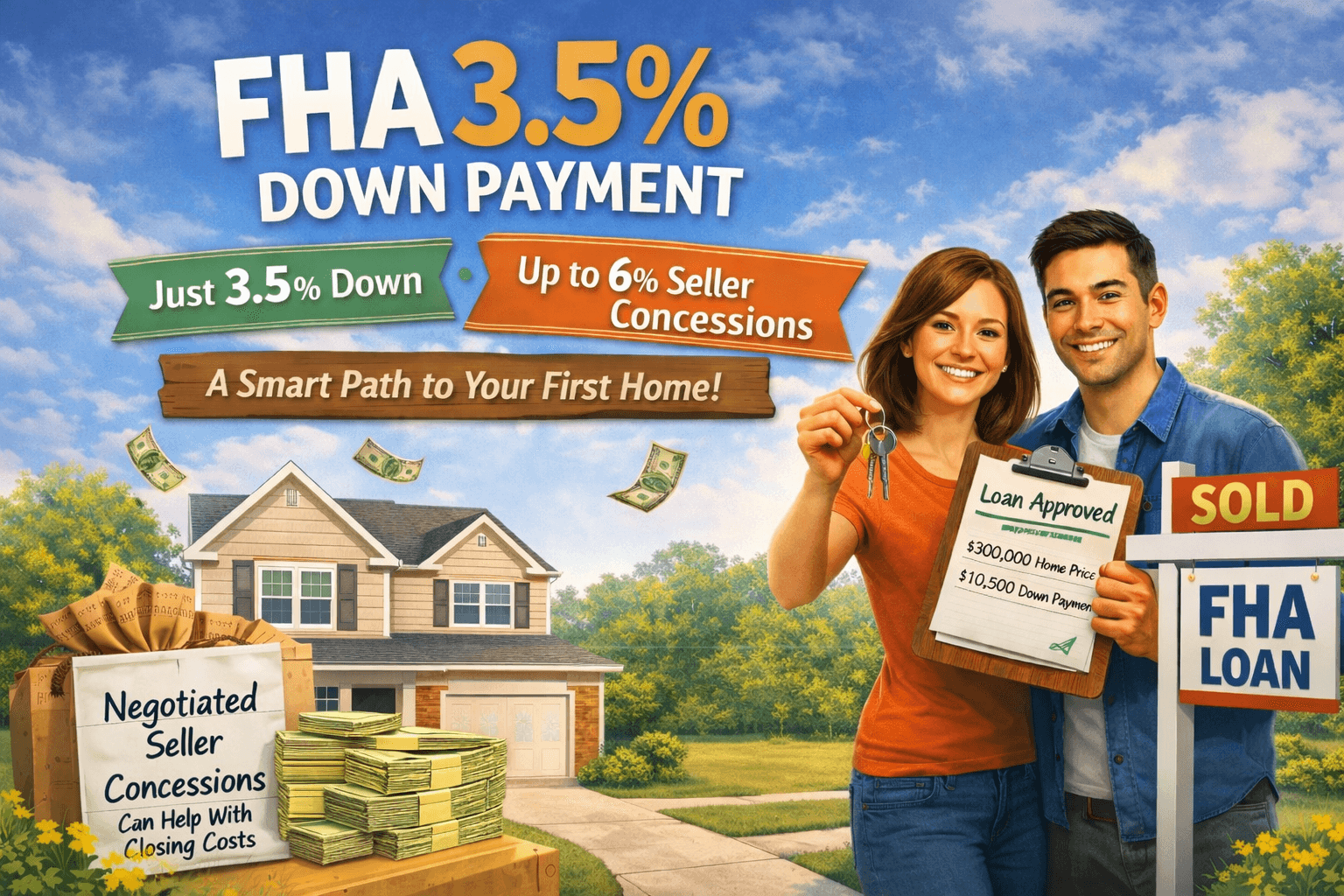

FHA 3.5% Down Payment Mortgage

A Simple Guide for First-Time Homebuyers

What is an FHA mortgage?

An FHA mortgage is a home loan insured by the Federal Housing Administration.

Because the loan is insured, lenders can offer more flexible guidelines compared to many traditional loans.

Bottom line: FHA loans are designed to help people become homeowners—even if they don’t have perfect credit or a large down payment.

What does “3.5% down” mean?

The down payment is the portion of the purchase price you pay upfront.

With an FHA loan, many buyers can purchase a home with just 3.5% down, as long as they qualify.

Simple example

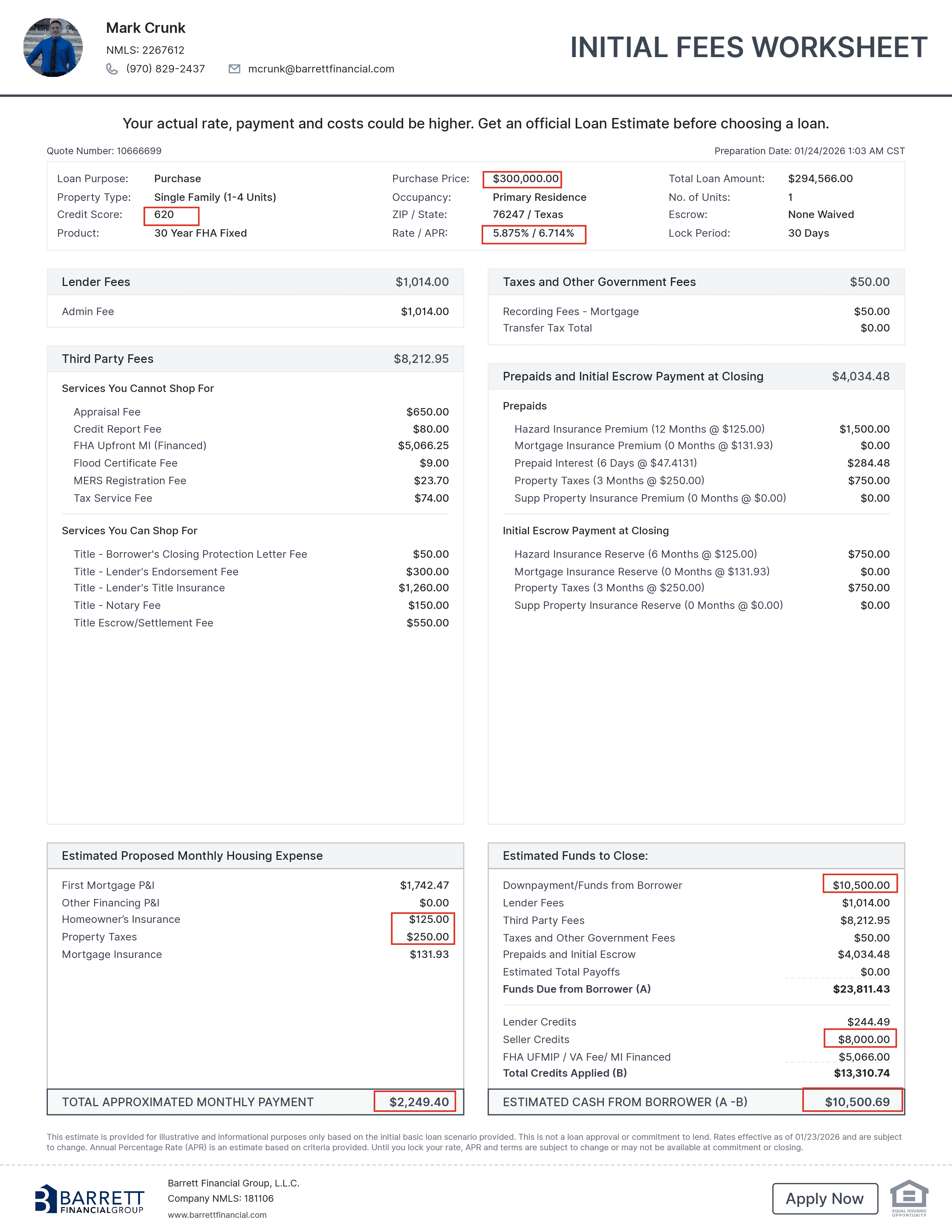

If the home price is $300,000:

- 3.5% down = $10,500

- The remaining amount is financed through the loan

Your down payment can come from:

- Personal savings

- A gift from a family member (following FHA rules)

- Certain approved assistance programs

One of the biggest advantages: up to 6% in seller concessions

This is one of the most powerful benefits of an FHA loan—and many first-time buyers don’t know it exists.

What are seller concessions?

Seller concessions are costs that the home seller agrees to pay on your behalf as part of the purchase contract.

With an FHA loan, you can negotiate up to 6% of the purchase price in seller concessions.

What can seller concessions be used for?

Seller concessions can be applied toward:

- Closing costs

- Prepaid items (like taxes and homeowners insurance)

- FHA upfront mortgage insurance

- Buying down the interest rate to lower your monthly payment

Important: Seller concessions cannot be used for your down payment, but they can dramatically reduce how much money you need out of pocket.

Why this matters for first-time buyers

In many cases, seller concessions can:

- Cover most or all closing costs

- Reduce cash needed at closing to a much smaller amount

- Help lower the monthly payment by buying down the rate

This is why many FHA buyers focus on total out-of-pocket cost, not just the purchase price.

Advantages of an FHA 3.5%

down payment mortgage

1) Low down payment

You don’t need 10–20% down to buy a home.

2) Up to 6% seller concessions allowed

This flexibility can significantly reduce upfront costs and make buying more realistic.

3) More flexible credit guidelines

FHA is often a good fit for buyers with limited or rebuilding credit (approval depends on the full loan profile).

4) Gift funds are allowed

Family members can help with the down payment when properly documented.

5) Competitive option for first-time buyers

For many buyers, FHA provides a clearer path to ownership when conventional loans are harder to qualify for.

Disadvantages of an FHA 3.5%

down payment mortgage

1) Mortgage insurance is required

FHA loans include:

- Upfront mortgage insurance (often financed into the loan)

- Monthly mortgage insurance, which increases the monthly payment

In many cases, this mortgage insurance lasts for the life of the loan if only the minimum down payment is made. Many homeowners later refinance into a different loan if it makes financial sense.

2) Monthly payment includes more than just the loan

Your full payment typically includes:

- Principal and interest

- Property taxes

- Homeowners insurance

- FHA mortgage insurance

- HOA dues (if applicable)

3) Property condition standards

Homes must meet FHA safety and livability guidelines, which can sometimes require repairs.

4) Loan limits apply

FHA has maximum loan limits that vary by county and can affect price range in higher-cost areas.

Who is a good fit for an

FHA 3.5% down loan?

This loan is often a great option if:

- You’re a first-time homebuyer

- You have limited savings but steady income

- You want the ability to negotiate seller help

- You prefer a predictable, structured loan option

The most important thing to understand

The real advantage of FHA isn’t just the 3.5% down—it’s how the loan allows you to combine a low down payment with seller concessions to reduce your total upfront cost.

The smartest move is to look at:

- Total cash needed to close

- Total monthly payment

- How seller concessions can be used strategically