Zero Down USDA Home Renovation Mortgage

Buy a home and renovate it—without a down payment (in eligible rural areas)

If you’re looking at a home that has “good bones” but needs updates, a USDA renovation mortgage may let you purchase the property and finance eligible improvements in one loan—with 0% down for qualified buyers.

This program can be a strong fit for buyers who want to move into a home they can improve over time, while still getting the advantages USDA loans are known for: competitive interest rates and more flexible down payment requirements compared to many conventional options.

The Big Misunderstanding: “Zero Down” Doesn’t Mean “Zero Cost”

A USDA renovation mortgage can offer 0% down payment, but closing costs still apply—just like with any mortgage.

Typical closing costs may include:

- Lender fees (origination/underwriting)

- Appraisal and credit report

- Title insurance, escrow, recording fees

- Prepaid items (homeowner’s insurance, taxes, etc.)

How many buyers handle closing costs

The most common strategy is negotiating seller concessions.

✅ USDA allows seller concessions up to 6%

Important: the 6% is based on the initial purchase price, not the after-renovation or “as-completed” value.

Seller concessions can often be used to help cover:

- Closing costs and prepaid items

- Certain lender fees (as allowed)

- Potential interest rate buydowns (when available and permitted)

(Any credits are subject to program rules and what’s allowed on your Loan Estimate and Closing Disclosure.)

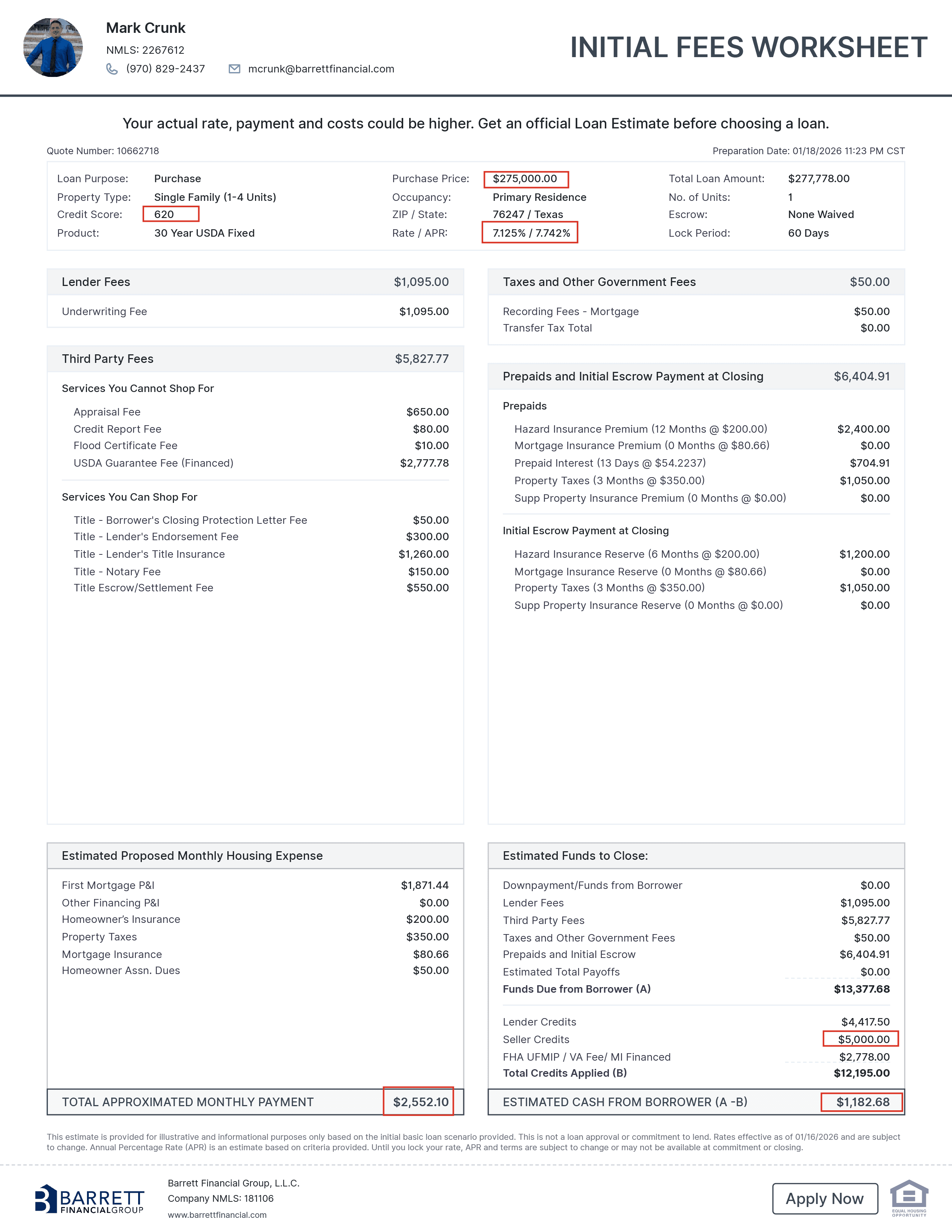

Here is a sample loan scenario based upon a home in a USDA eligible area that needed some updates and repairs with a 620 credit score and interest rates as of 1/16/26. The home was listed at $165,000 and budgeted $95,000 for the renovation and had a $15,000 reserve account set up making the total loan amount of $275,000.

USDA Guidelines Still Apply (Even With Renovations)

Because this is still a USDA-backed mortgage, borrowers must meet standard USDA eligibility rules, including:

- Property must be in an eligible USDA area

- Household income must be within USDA limits

- Stable, documentable income

- Debt-to-income ratios (DTI) must fall within USDA guidelines

- The home must meet property standards (and the renovation scope must bring it to an acceptable standard)

USDA programs are popular because interest rates are often favorable compared to conventional loan programs, but the trade-off is that income limits and DTI requirements are usually enforced strictly.

Minimum Credit Score: 580

(But Here’s the Real-World Truth)

Many lenders require a minimum 580 FICO for USDA eligibility, but lower scores often mean:

- manual underwriting,

- more documentation,

- and a greater need for compensating factors.

Why scores over 620 matter

In many cases, FICO scores 620+ tend to receive:

- better interest rates, and

- easier qualification standards (because the file is typically stronger from an underwriting perspective).

Compensating Factors (Examples)

If your score is on the lower end (especially under ~620), having one or more compensating factors can help strengthen the overall loan profile.

Common examples include:

- Strong cash reserves (money left over after closing)

- Low or conservative debt usage relative to income

- Stable job history (consistent employment and reliable earnings)

- Minimal payment shock (new payment isn’t dramatically higher than current rent)

- Verified history of on-time housing payments (rent/mortgage history)

- Additional household income that’s stable and documentable

- Low DTI compared to maximum allowed (more “room” in the ratio)

Compensating factors don’t guarantee approval, but they can make a meaningful difference when the loan file is close to the edge of the guidelines.

Automatic Disqualifiers to Know Up Front

While each lender’s overlays can vary, these are common items that can automatically disqualify a borrower from USDA financing (or stop the loan until resolved):

- Household income exceeds USDA income limits for the area/household size

- Property not located in an eligible USDA area

- Borrower not able to document stable, ongoing income

- Excessive DTI that doesn’t meet USDA requirements

- Significant recent credit events (examples may include unresolved collections, major late payments, recent bankruptcies/foreclosures within restricted timeframes, depending on guidelines and lender overlays)

- Federal debt delinquencies or unresolved government liens

- Active repayment issues (such as unresolved judgments that must be addressed prior to closing)

- Ineligible property condition that cannot be brought up to standards through the renovation scope

If you’re unsure whether something applies to you, it’s usually better to run a quick pre-check before you shop heavily—because USDA is very specific about eligibility.

Renovation Basics: What Can Be Improved?

Renovation eligibility depends on the lender/investor and program structure, but commonly financed improvements may include items like:

- roofing, siding, windows

- flooring, paint, kitchen/bath updates

- HVAC, plumbing, electrical repairs

- accessibility improvements

- well/septic repairs (where allowed)

- health/safety issues and deferred maintenance

The key is that the renovation plan typically needs to bring the home to acceptable standards and support livability and durability—not luxury upgrades.

Who This Program Is Best For

This can be a great fit if you:

- want zero down and qualify under USDA income limits

- are buying in a USDA-eligible area

- found a home that needs updates but is a great long-term value

- want one loan instead of a purchase loan plus separate renovation financing

Quick FAQ

Is it really zero down?

Yes—down payment can be 0%. But you should still plan for closing costs, unless they’re covered through seller concessions and/or other allowable credits.

Can seller concessions cover everything?

Sometimes, depending on purchase price, closing costs, and what’s allowed—but remember the cap is up to 6% of the purchase price, not the after-renovation value.

Do I have to meet USDA income limits?

Yes. USDA income limits are a core eligibility requirement and usually strictly applied.

Is a 580 score enough?

580 may meet minimums, but approval is not automatic. Lower scores often need strong compensating factors, and many borrowers find 620+ puts them in a much better position for rates and approval.

Want to see if you qualify?

If you’re thinking about buying a home that needs work and using a 0% down USDA renovation mortgage, I can help you:

- check USDA property eligibility,

- estimate your income limit and DTI comfort zone,

- and map out the best strategy for seller concessions and closing costs.

Reach out for a quick personalized scenario review.

Call or Text 970-829-2437