Save Smart While You Wait to Buy a Home: HYSA vs. Roth IRA

If you’re not quite ready to buy a home—whether because of credit score, income stability, or simply waiting for the right market—this doesn’t mean you should sit idle. The time you spend preparing is a golden opportunity to build both your down payment and your long-term financial security.Two powerful tools stand out:High-Yield Savings Accounts (HYSA) – safe, steady, and liquid.Roth IRA – flexible for home purchases and designed to grow your retirement nest egg.

⚠️ Disclaimer: I am not a financial advisor. Investing involves risk, and past performance does not guarantee future results. Please consult with a licensed financial professional before making investment decisions.

Why Saving a Little Every Week Matters

Let’s put things in perspective with a simple routine: saving $15 a day, Monday through Friday. That’s $75 a week, or $3,900 a year. Over five years, you would contribute $19,500—and with compounding interest, that money grows.

But this isn’t just about $15 a day. The bigger lesson is getting into the habit of saving or investing 10–15% of your paycheck. If that feels out of reach, don’t get discouraged—every dollar matters. Even small, consistent contributions can snowball into something meaningful over time. What’s important is developing the habit and building financial discipline.

And if you can, pass this mindset on. Teaching your children or grandchildren the value of saving early and taking advantage of compounding interest could set them on a lifelong path to financial security.

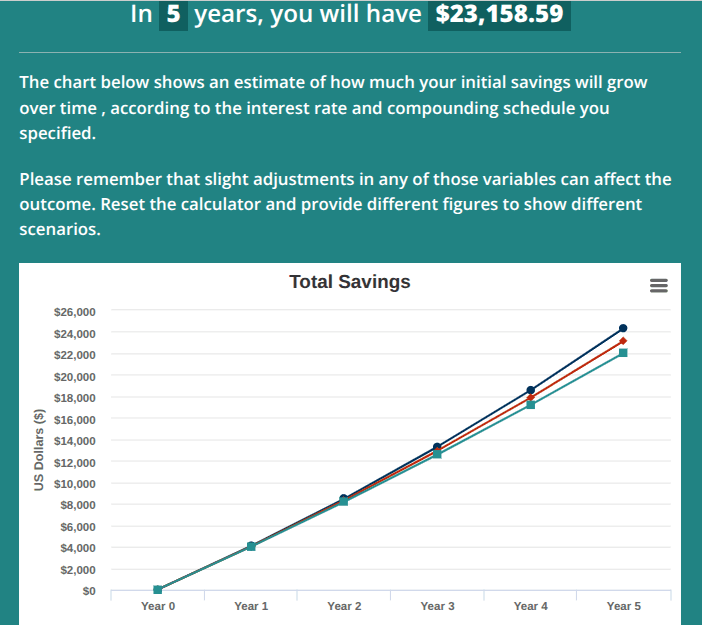

How Much Can $15 a Day (5 Days a Week) Become in 5 Years?

Total contributions:

$75 × 52 weeks × 5 years = $19,500

Growth Results (After 5 Years)

High-Yield Savings (3.5% APY) → $21,270

Roth IRA @ 7% return → $23,189

Roth IRA @ 9% return → $24,355

Net Growth (Earnings Only)

HYSA: +$1,770

Roth IRA (7%): +$3,689

Roth IRA (9%): +$4,855

Pros & Cons of Each Option:

High-Yield Savings Account (HYSA)

Pros

FDIC insured, safe from market volatility

Instant access to funds (perfect if you need all of it for closing)

No fees or minimums at places like Capital One 360 Performance Savings (currently ~3.5% APY)

Cons

Lower growth compared to investing

Rates may change with the economy

Roth IRA

Pros

Contributions can be withdrawn at any time tax- and penalty-free

Up to $10,000 in earnings can be used penalty-free for a first-time home purchase

Much stronger long-term growth potential (historical averages ~7–9% annually)

Continues building wealth for retirement even after the home purchase

Cons

Subject to market risk; balances may fluctuate

Contribution limits ($7,000/year under 50; $8,000 if over 50)

Rules apply to accessing earnings—best used if you can leave most invested

Side-by-Side: 5-Year Snapshot

| Strategy | Ending Balance | Growth Over Contributions | Liquidity |

|---|---|---|---|

| HYSA (3.5% APY) | $21,270 | +$1,770 | Very high |

| Roth IRA (7%) | $23,189 | +$3,689 | Contributions liquid; earnings limited |

| Roth IRA (9%) | $24,355 | +$4,855 | Contributions liquid; earnings limited |

Final Thoughts

The numbers prove it: even with modest contributions, the power of compounding interest adds up quickly.

If your priority is safety and guaranteed access, a high-yield savings account is a strong choice—especially for short-term goals like a down payment.

If you’re aiming for greater growth while still keeping the option to use funds for a first-time home, a Roth IRA may be the smarter path. And even better, it keeps working for you long after you’ve purchased your home.

Below is a hypothetical example of a potential five year investment based upon a $15 per day on a 5 day week timeline invested on a monthly basis at about 7% return on investment. I personally use SoFi because of it's ease of use. Here is a link if you want to open an account and get $25 in a stock for opening an account. It's completely free and when signing up under my link, full disclaimer, I also get a small investment added to my account:

One of the things that I love about SoFi is the ability to sign up with a robotrader so if you're not a savvy investor, you can sign up for robotrader and it will invest for you based upon your investment goals. Feel free to contact me if you have any questions or need assistance with setting up your free SoFi Account.

Remember, I am not a financial advisor. Investing involves risk, and past performance does not guarantee future results. Please consult with a licensed financial professional before making investment decisions.

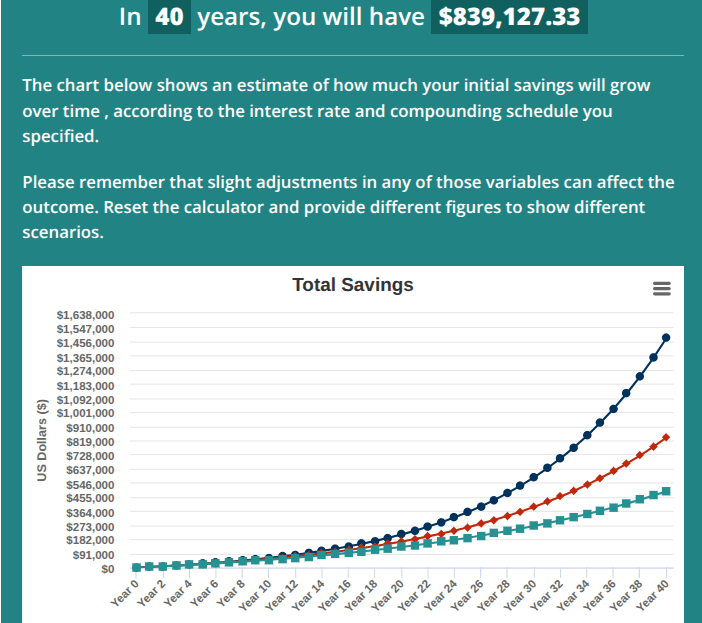

Even if you don't decide to purchase a home, saving for your retirement is so important! Take a look at the next hypothetical scenario based upon investing the same amount over a 40 year period. Look how much you could potentially have if you are able to achieve a 9% return on your investment!:

If at some point you are wanting to purchase a home and want to get mortgage ready and pre-qualified, I would love to assist you achieve your dream of homeownership! Feel free to reach out to me at 970-829-2437, call or text!

Purchase a Home

Whether you're buying your first home or your dream home, we have a mortgage solution for you. Get your custom rate quote today.

Refinance your Home

We're committed to helping you refinance with the lowest rates and fees in the industry today. Getting started is quick and easy.

Apply Today

Our secure application is a few quick questions that takes about 7-10 minutes to complete and is required for a “Pre-Approval”. Get started today!