Why Would Anyone Buy a Home in Today’s Market?

It’s a fair question.

The numbers don’t lie:Median rent for a 3-bed/2-bath single-family home: $2,100/month.

Estimated FHA mortgage (PITI + MIP) on a $350,000 home at 6.125%/6.958% APR: $2,730/month.

On paper, renting looks cheaper — you’re saving about $630 per month. So why in the world would anyone buy a home right now?

Renting vs. Buying: Short Term vs. Long Term

Renting: Over 5 years at $2,100/month, you’ll spend $126,000. At the end, you own nothing.

Buying: Even though the monthly payment is higher, after 5 years you’ll have built equity, plus the home could appreciate in value. At just 2% annual growth, a $350,000 home could be worth nearly $386,000 in 5 years — about $36,000 in appreciation on top of your loan paydown.

Rent is cheaper today, but ownership builds tomorrow’s wealth.

The Advantage of Owning

Stability: Your mortgage payment (principal + interest) stays fixed. Renters risk annual increases.

Refinance Opportunity: Rates won’t stay this high forever. Homeowners can refinance later. Renters cannot.

Generational Wealth: After 30 years, a renter could easily spend $1 million+ in rent. A homeowner has a paid-off home potentially worth hundreds of thousands of dollars — an asset to pass down.

But What If You Can’t Afford to Buy Right Now?

That’s a real concern for many families today. So the question becomes: Now what?

Instead of sitting on the sidelines waiting for prices or rates to fall (which may or may not happen), you can start building a plan.

Most people think of saving for a down payment in a simple savings account. But there’s another option: investing for your down payment and closing costs.

Why Investing Can Work Better Than Just Saving

Savings Account: Safe but slow. Even a high-yield savings account might give you 3.5% interest. There are other high yield savings that may give you a higher yield but make sure that you read the fine print!

Investing (like through a Roth IRA or brokerage account): While there are risks, long-term investing historically has returned 7–10% annually. That kind of growth can help your money work harder.

For example, let’s say you set aside $500/month:

In a savings account at 3.5% interest, you’ll have about $26,500 after 4 years.

Invested at 8% return, you could have closer to $29,000–30,000 — enough to cover a down payment and closing costs on many starter homes.

The Bottom Line

Right now, renting looks cheaper. But buying creates wealth, stability, and ownership over time.

If you can’t afford to buy today, that doesn’t mean you should do nothing. It means you should:

Build credit so you qualify for the best loan programs.

Create a budget that allows you to consistently set aside money.

Invest what you can, so your money grows instead of sitting idle.

Five years from now, you’ll either look back at tens of thousands spent on rent — or you’ll be holding the keys to a home that’s building wealth for you and your family.

Final Thought

Would you like to run the numbers based on your specific situation and location? Reach out to me. With today’s motivated sellers, we may be able to get you into a home and buy down your interest rate for very little out-of-pocket expense!

And if you’re not quite ready to buy and don’t know where to start saving or investing for your future, I may be able to point you in the right direction. (I am not a licensed financial adviser, but I can help connect you with tools and resources that could get you started on the right path.)

Disclaimer: I am not a licensed financial advisor, tax professional, or investment advisor. The information provided here is for educational purposes only and should not be considered financial, legal, or investment advice. Before making any financial decisions, you should consult with a licensed professional who can review your specific situation.

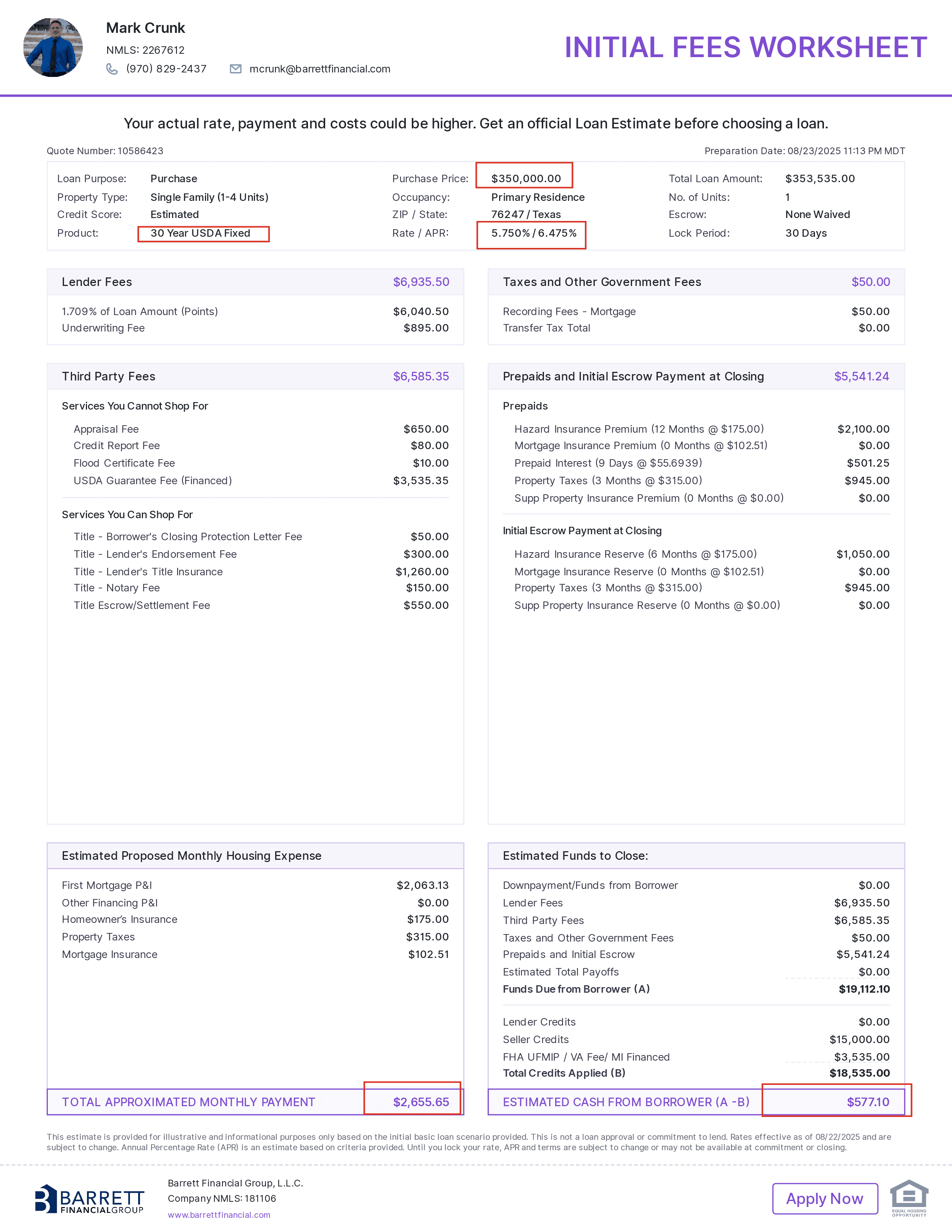

Below is a hypothetical loan scenario based upon a 620 credit score and interest rates as of 6/22/25 using a zero down payment USDA home mortgage with a $350,000 purchase price and $15,000 in seller concessions and buying down the interest rate to 5.75% with an APR of 6.475% and total cash to close is less than $1,000!

Purchase a Home

Whether you're buying your first home or your dream home, we have a mortgage solution for you. Get your custom rate quote today.

Refinance your Home

We're committed to helping you refinance with the lowest rates and fees in the industry today. Getting started is quick and easy.

Apply Today

Our secure application is a few quick questions that takes about 7-10 minutes to complete and is required for a “Pre-Approval”. Get started today!