I am not a licensed financial advisor. This content is for educational purposes only and should not be considered financial advice. Investing involves risk, including the possible loss of principal. Always conduct your own research and consult with a qualified financial professional before making investment decisions.

How Just $15 a Day Can Change Your Entire Future

If you’re 18 and just starting your first job, buying a home might feel like a lifetime away. Retirement? That’s even harder to picture. But what if I told you that by saving just $15 a day, 5 days a week, you could buy your first home shortly after college and retire a millionaire?

The $15-a-Day, 5 Days a Week Plan

Let’s break it down:

$15/day × 5 days/week × 52 weeks/year = $3,900/year

Divide that by 12 months and you’re investing about $325/month

Instead of letting that money slip away on fast food, streaming subscriptions, or impulse buys, you put it into a Roth IRA — a retirement account that grows tax-free.

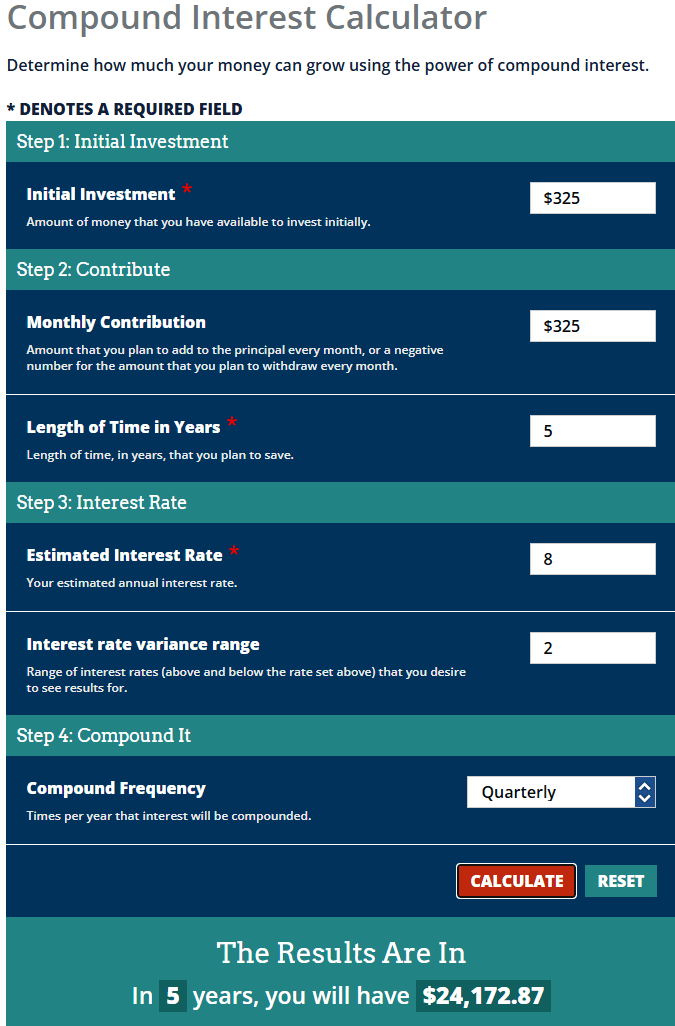

Step 1: The 5-Year Home Fund

If you invest $325/month into a Roth IRA earning 8% interest, after just 5 years, you could have about:

💰 $24,000

Now imagine this: At age 23, you take $20,000 from that account for a down payment on your first home (you can withdraw contributions penalty-free for a first-time home purchase). That leaves you with around $4,000 still invested in your Roth IRA — and you keep contributing monthly.

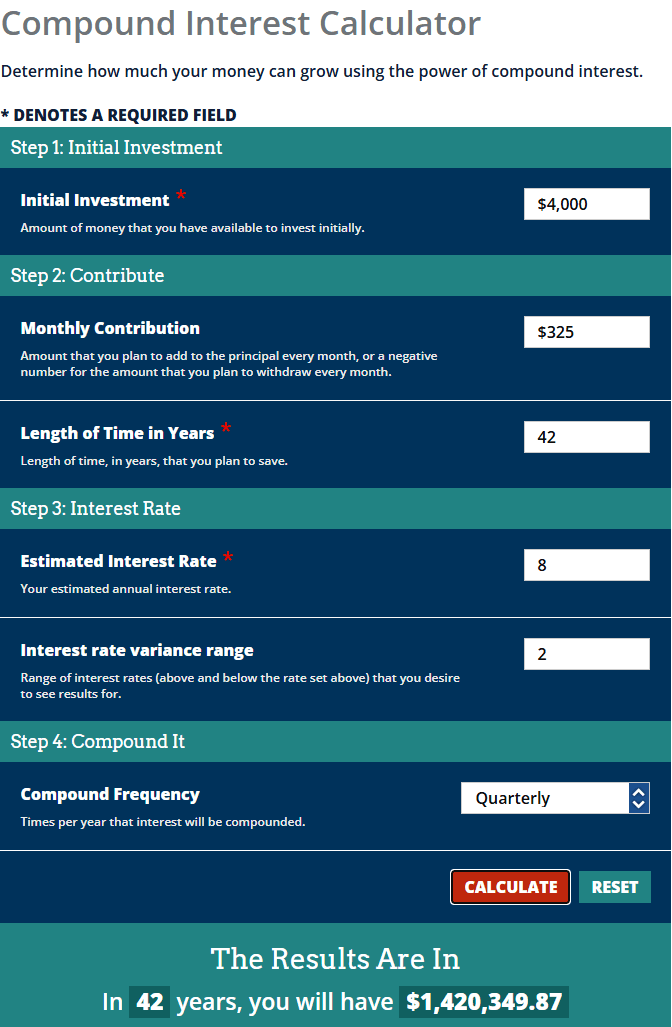

Step 2: The Millionaire Retirement Plan

From age 23 to 65, you keep investing your $325/month and let your money grow at 8% annually. By the time you retire, your Roth IRA could be worth about:

💰 $1,420,000

That’s over 1.4 million dollars completely tax-free — and that’s on top of the equity you’ve built in your home over the years, it will probably be paid off by then and maybe the equity in the home could help you to buy even more houses for income property!

Step 3: Building Generational Wealth

Maybe you keep that first home as a rental property when you buy your second. Maybe you repeat the process again. By starting early, you’re not just buying a house — you’re setting yourself up for generational wealth that can change your family’s future.

Bottom line: $15 a day is less than the cost of lunch. But if you invest it wisely, it can give you a home in your 20s and a millionaire’s retirement in your 60s.

📌 Start now. Your future self will thank you.

What Does History Tell Us?

1. S&P 500 (as a proxy for stock-heavy Roth IRAs)

- Since 1926, the compound annual total return of the S&P 500—including dividends—is about 9.8% per year (around 6% after adjusting for inflation) Investopedia+15Wikipedia+15Reddit+15.

- From 2014 to 2024, the index’s average annualized return was 11.3%, which equates to approximately 8% after inflationU.S. News Money.

2. Typical Roth IRA Performance

- Depending on how you invest, Roth IRAs tend to average 7% to 10% annual returns, depending on the asset mix Wikipedia+9SmartAsset+9Empower+9.

- Some financial tools and calculators assume average Roth IRA returns closer to 6%—not far off from conservative real-life expectations Empower.

3. Compounding Power at 8%

- Examples using a steady 8% return show how compound growth accelerates savings: by year 10, interest gains can far exceed annual contributions Investopedia+15Investopedia+15Investopedia+15.

- Even if contributions stop after 20 years, the account continues to grow significantly thanks to compounding Investopedia.

4. Long-Term Equity Returns (Beyond Stocks)

- Over long historical spans, U.S. stocks have delivered real (inflation-adjusted) returns around 6.8% per yearWikipedia+2Wikipedia+2.

- More globally diversified portfolios historically net 3%–6% in real returns, depending on the era and region Wikipedia.

5. Rolling 20-Year Performance (via Reddit insight)

- One popular personal finance discussion noted:

“Annual returns were 8% or more in 75% of all rolling 20-year observations. They were 10% or higher 56% of the time.” Investopedia+2Investopedia+2Reddit+1

“Annual returns were 8% or more in 75% of all rolling 20-year observations. They were 10% or higher 56% of the time.” Investopedia+2Investopedia+2Reddit+1

Summary Table

Investment Type / Scenario Historical Return Estimate Notes S&P 500 Total Return (1926–Present) ~9.8% (6% real) Includes dividends Wikipedia+1 S&P 500 (2014–2024) ~11.3% nominal (8% real) Recent decade data U.S. News Money Roth IRA (varied asset mix) 7%–10% Based on typical diversified allocations SmartAsset Conservative Roth IRA ~6% Lower-risk portfolios NerdWallet U.S. Stocks (long-term, real returns) ~6.8% Historical average over many decades Wikipedia Global Market Portfolio (real returns) ~4%–6% Varies by era Wikipedia Rolling 20-Year Stock Market Returns ≥8% in 75% of cases; ≥10% in 56% Reddit-sourced long-term performance insight Reddit

| Investment Type / Scenario | Historical Return Estimate | Notes |

|---|---|---|

| S&P 500 Total Return (1926–Present) | ~9.8% (6% real) | Includes dividends Wikipedia+1 |

| S&P 500 (2014–2024) | ~11.3% nominal (8% real) | Recent decade data U.S. News Money |

| Roth IRA (varied asset mix) | 7%–10% | Based on typical diversified allocations SmartAsset |

| Conservative Roth IRA | ~6% | Lower-risk portfolios NerdWallet |

| U.S. Stocks (long-term, real returns) | ~6.8% | Historical average over many decades Wikipedia |

| Global Market Portfolio (real returns) | ~4%–6% | Varies by era Wikipedia |

| Rolling 20-Year Stock Market Returns | ≥8% in 75% of cases; ≥10% in 56% | Reddit-sourced long-term performance insight Reddit |

Takeaway

An 8% average annual return in a Roth IRA—especially one richly invested in equities—is well within historical norms, particularly over long periods. Over decades of compounding and disciplined contributions, hitting 8% can lead to powerful wealth accumulation (which your blog examples beautifully illustrate).

That said:

- Past performance doesn’t guarantee future results, and short-term volatility is real.

- While historical returns are encouraging, realizing those gains depends on consistent contributions, asset allocation, and time in the market.

Here is a link to sign up for SOFI and receive $25 worth of your favorite stock or investment when signing up!

FULL DISCLOSURE:

I RECEIVE COMPENSATION WHEN YOU SIGN UP FOR A SOFI ACCOUNT

Don't forget to reach out to me when you are ready to make that first home purchase!

Purchase a Home

Whether you're buying your first home or your dream home, we have a mortgage solution for you. Get your custom rate quote today.

Refinance your Home

We're committed to helping you refinance with the lowest rates and fees in the industry today. Getting started is quick and easy.

Apply Today

Our secure application is a few quick questions that takes about 7-10 minutes to complete and is required for a “Pre-Approval”. Get started today!