Income — Not Savings — May Very Well Be The Biggest Barrier To Homeownership In 2025

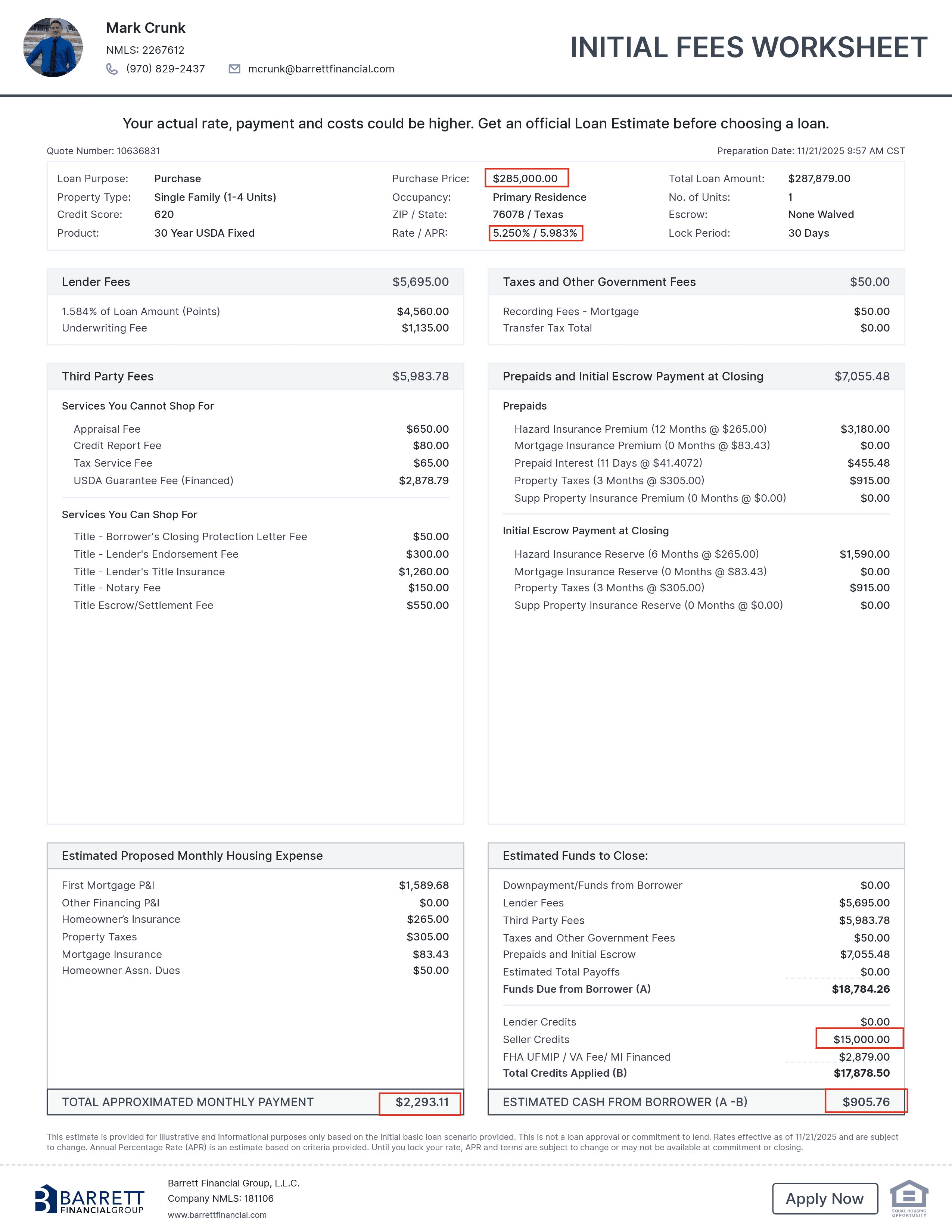

A Real Hypothetical USDA Mortgage Case Study Using a $285,000 Home in Wise County, Texas Most first-time buyers believe the hardest part of buying a home is saving for the down payment. But in today’s market—with higher rates, strict underwriting rules, and rising taxes—the real obstacle is not cash… it’s income.Even when a buyer can get into a home with less than $1,000 at closing, and even when buying dramatically increases their net worth compared to renting, many families still cannot qualify because their income doesn’t meet USDA requirements or DTI guidelines.This real-world Texas scenario proves it.

🏡 USDA Home Purchase Scenario (Wise County, Texas)

Purchase Price: $285,000

Interest Rate: 5.250%

APR: 5.983%

Cash to Close:$905.76

Loan Program: USDA (0% down)

Monthly Payment Breakdown

| Item | Amount |

|---|---|

| Principal & Interest | $1,589.68 |

| Property Taxes | $305 |

| Homeowners Insurance | $265 |

| HOA | $50 |

| Total Monthly Payment | $2,293.11 |

Comparable Rent in Same Neighborhood

$1,925 per month

Difference: $368.11 more per month to own

Even with that slight increase, the wealth difference over time is significant — but the income barrier is even bigger.

📈 5-Year Wealth Comparison: Buyer vs. Renter

🏡 Homeowner Equity After 5 Years

Home value after 5 years at 1.5% appreciation:

$285,000 → $306,776Loan balance after 5 years:

$265,278.56Equity gained:

$306,776 − $265,278.56 = $41,497.44

👤 Renter Who Invests Savings at 8%

Renter invests their monthly savings of $368.11 at 8% annual return (compounded monthly):

5-year value = approx. $22,100

💰 Net Worth After 5 Years

| Scenario | Net Worth |

|---|---|

| Buyer | $41,497.44 |

| Renter | ≈ $22,100 |

| Homeowner Advantage | +$19,397.44 |

Buying still produces nearly $20,000 more wealth over five years — even when renting and investing every dollar saved.

But again…

None of this matters if the buyer cannot qualify due to income.

🚫 Income Requirements: A Very Real Obstacle

To qualify for this USDA mortgage, borrowers must meet USDA’s front-end DTI rules.

With Strong Compensating Factors (32% DTI Front-End)

Required income:

$2,293.11 ÷ 0.32 = $7,166.00 per month

= $85,992 per year

Without Compensating Factors (29% DTI Front-End)

Required income:

$2,293.11 ÷ 0.29 = $7,907.31 per month

= $94,887.72 per year

Now compare this with USDA income limits.

📊 Current USDA Income Limits (Wise County, Texas)

✔ 1–4 person household:$119,850

✔ 5–8 person household:$158,250

✔ With compensating factors ($85,992/year needed):

This income meets USDA limits.

✔ Without compensating factors ($94,887.72/year needed):

This income also meets USDA limits,

but the back-end DTI becomes the problem.

If the borrower has more than $1,000/month in car payments, credit cards, or other debts, they will fail USDA DTI, even though they stay under the county income limit.

This is why USDA loans fail most often not because of income limits —

but because income vs. debt cannot meet DTI rules.

🧩 What Are Strong Compensating Factors?

Most buyers have no idea what qualifies them for the 32% DTI exception.

Here are real, lender-recognized compensating factors:

✔ Higher credit score (680+)

✔ Very low existing monthly debt

✔ Verified on-time rental history

✔ Cash reserves after closing

✔ Stable employment (2+ years same field)

✔ Additional household income not used for qualifying

✔ Strong residual income

✔ Low payment shock (current rent close to new payment)

✔ Significant retirement or savings balances

When these are present, underwriters may approve a higher DTI — and that often determines whether the loan is approved or denied.

🔧 Alternate Path: FHA Loan

If the home is not in an eligible USDA area or the borrower:

exceeds USDA DTI guidelines, or

lacks compensating factors, or

has fluctuating income, or

has too much debt

…the next option is FHA.

FHA Highlights:

3.5% down payment

Down payment can be borrower funds or a gift

Gift cannot be a loan from a family member

Higher DTI caps than USDA

No county income limits

Does not need to be limited to a USDA eligible location

However:

FHA requires $9,975 down on this home

Payment might be higher

FHA mortgage insurance lasts longer

It’s a workable option — but not as affordable as USDA.

💡 Why Cash to Close Was Only $905.76

The Power of Smart Seller Concessions

This scenario used $15,000 in seller concessions to reduce closing costs and interest rate.

How it worked:

Home had recently dropped $10,000

Buyer offered to return price to original level

Then negotiated $15,000 total concessions

$10,000 from restored price

$5,000 additional concessions

This made it possible to:

Buy the rate down to 5.250%

Cover nearly all closing costs

Reduce cash-to-close to under $1,000

This is an outstanding, rare scenario —

but it still requires the income to qualify.

🧨 Final Takeaway: Income Is the Real Barrier, Not Cash

This Wise County scenario makes it clear:

✔ Buying builds ~$41,497 in equity

✔ Renting + investing builds ~$22,100

✔ Buying wins by ~$19,397

✔ Cash to close was under $1,000

✔ Seller concessions made the rate and closing costs possible

Yet most families still can’t qualify because:

They don’t earn $7,166–$7,907 per month

They have more than $1,000 in monthly debt

They lack the compensating factors to stretch their DTI

They don’t understand USDA income rules

Their income is too unstable to be used for qualification

Secondary income takes 12–24 months before it counts

This is why lack of income is one of the true gatekeepers of homeownership in 2025.

Families who understand this and begin planning now —

improving credit, stabilizing income, reducing debt, and building compensating factors —

can position themselves to qualify for a home in the next 12 to 24 months.

If you would like to discuss your unique scenario and help to prepare for future homeownership, feel free to reach out to me.

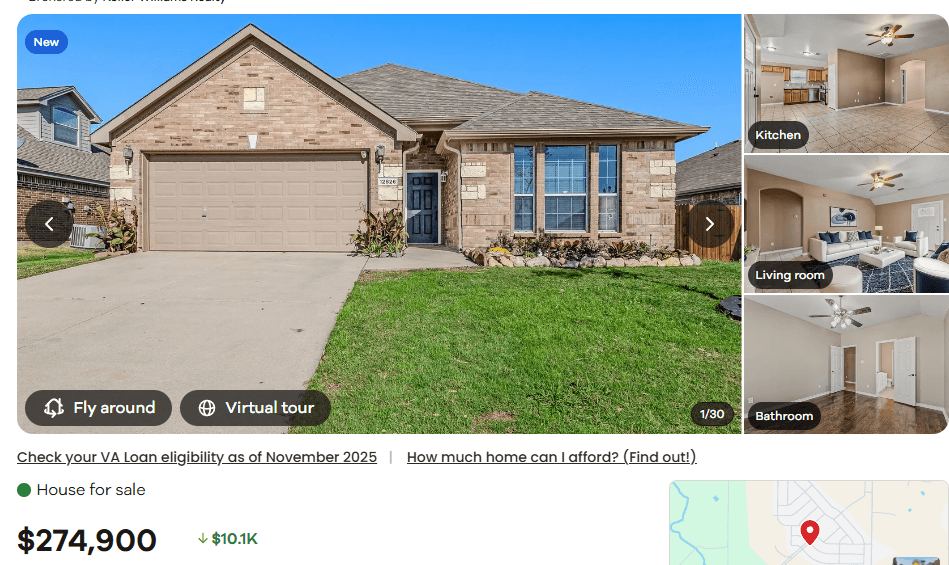

Home for sale used for this scenario. As of 11/21/25, this home was available for sale listed at $274,900 with a $10,000 price reduction.

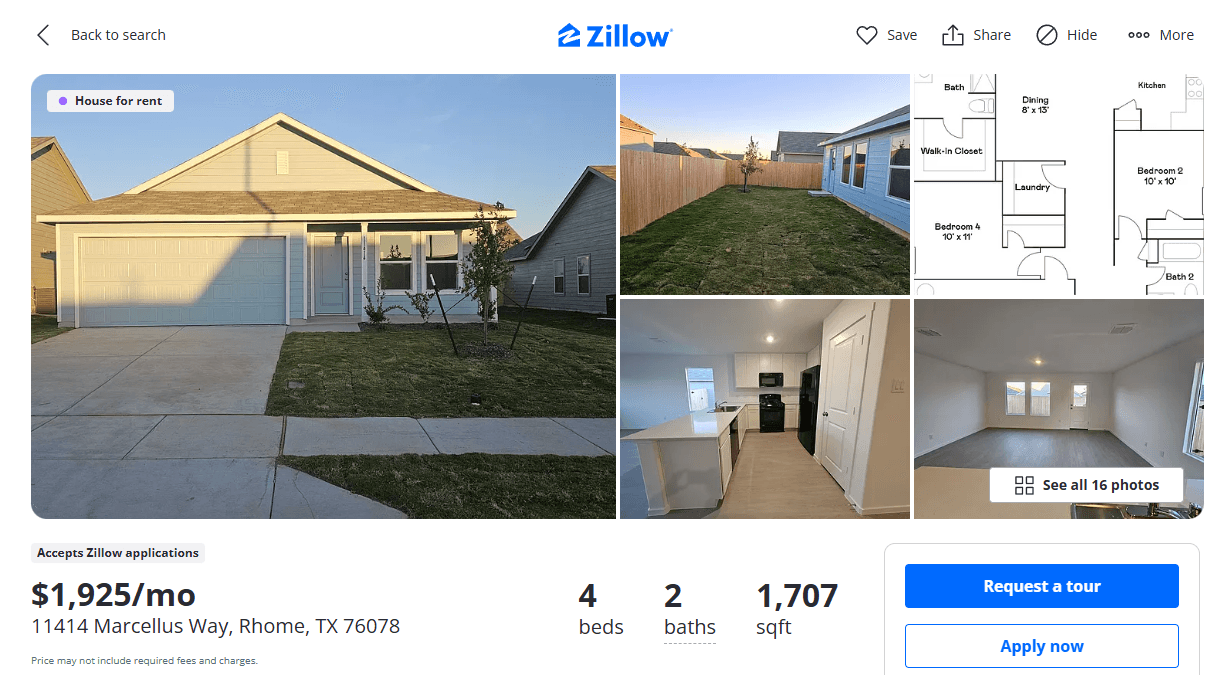

Home for rent used in this scenario. As of 11/21/25, this home was available to rent for $1,925.00 per month and is in the same neighborhood as the home for sale.

This is the actual hypothetical loan scenario based upon a FICO score of 620 and rates as of 11/21/25

Purchase a Home

Whether you're buying your first home or your dream home, we have a mortgage solution for you. Get your custom rate quote today.

Refinance your Home

We're committed to helping you refinance with the lowest rates and fees in the industry today. Getting started is quick and easy.

Apply Today

Our secure application is a few quick questions that takes about 7-10 minutes to complete and is required for a “Pre-Approval”. Get started today!