A Hypothetical DSCR Loan Scenario Based Upon A Real Property And A Qualified Buyer

(5-Year Breakdown)

What the Numbers For A Hypothetical DSCR Scenario Could Look Like With Property Management, Taxes, and Conservative Investing.

Why This Scenario Matters:

There’s no shortage of bold claims online about real estate investing — fast cash flow, early retirement, and “passive income” with no effort.

This blog is different. What follows is a Hypothetical DSCR rental scenario using: A modest brand-new home, Professional property management, Conservative rent increases, Modest appreciation, Disciplined investing of only the remaining cash flow, A high-income W-2 investor. No hype. Just math.

Although With This Hypothetical DSCR Loan Scenario Has Favorable Conditions In A Certain Market Area:

Disclaimer:

This scenario is provided for educational and illustrative purposes only. It is a hypothetical example and is not intended to represent a guarantee of profit or specific financial results. Actual results may vary and may be better or worse depending on factors including, but not limited to: market conditions, rental demand, property expenses, interest rates, property management costs, real estate negotiations, and individual financial circumstances. There is no guarantee that any investor will achieve the same or similar results, and investment performance is not guaranteed. This example is not a commitment to lend, not an offer to extend credit, and not a loan approval or pre-approval. All loan programs are subject to credit approval, underwriting guidelines, and lender requirements, which may change without notice.

Prospective investors should consult with their CPA, tax advisor, financial advisor, and real estate professionals before making any investment decisions.

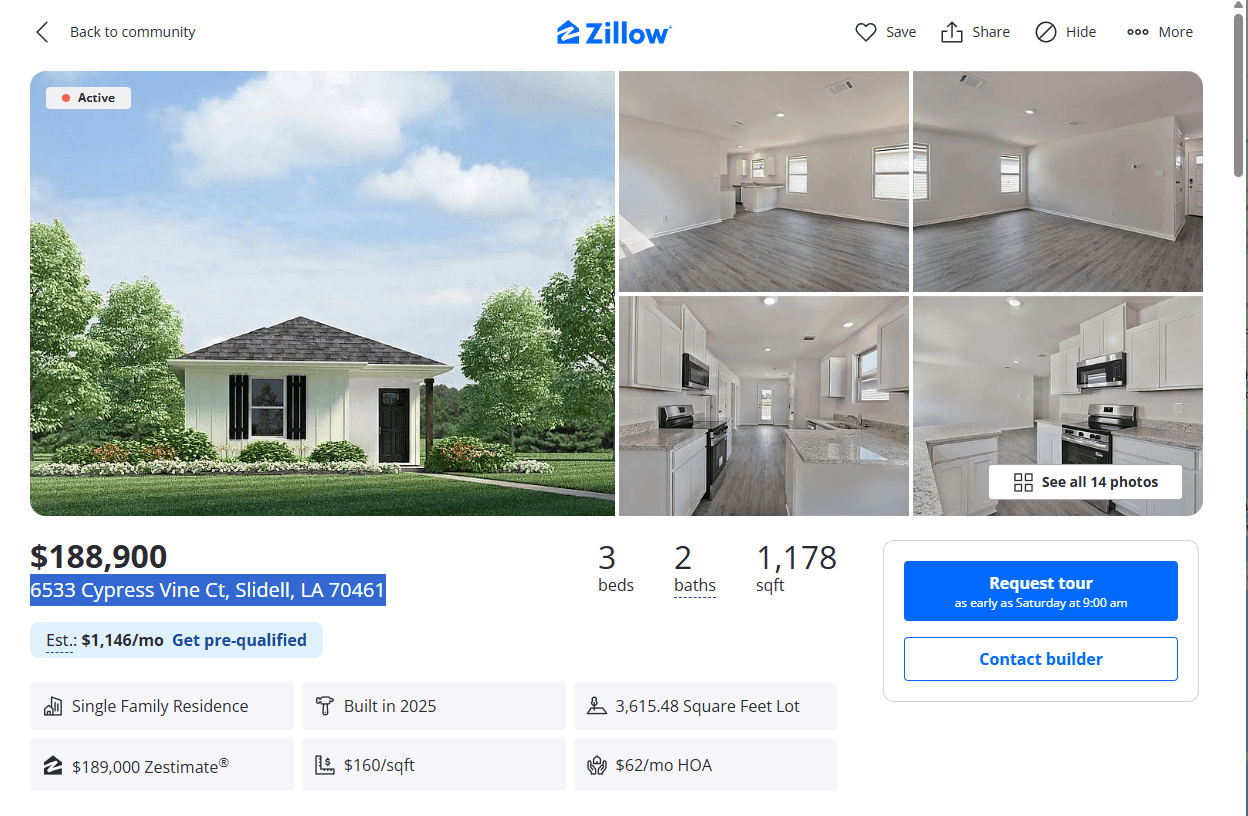

The Property & Loan Setup

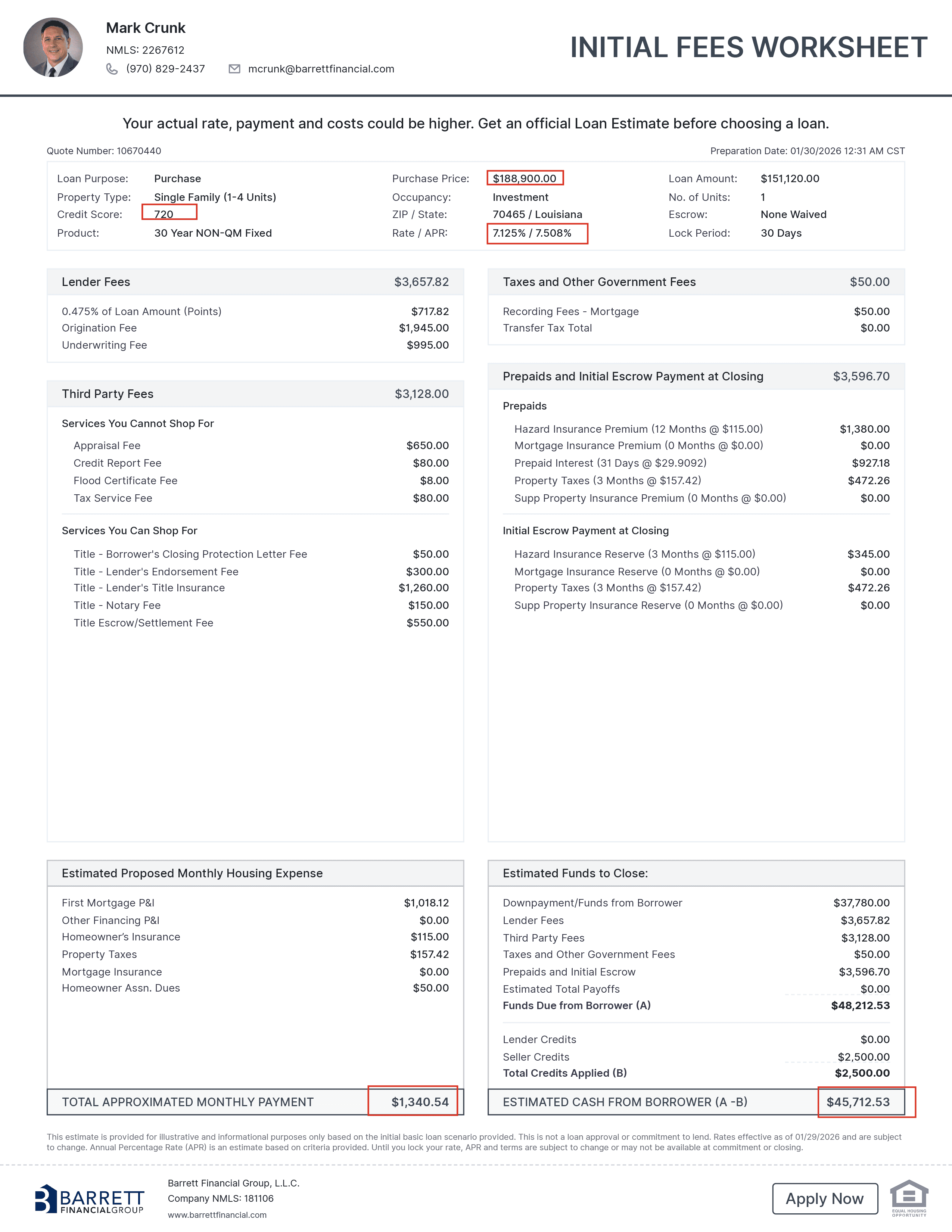

This Home Was Available As of 1/30/2026. The Builder Was DR Horton And In This Hypothetical Scenario, We Would Offer A Purchase Price Of $188,900 And Ask For $2,500 To Help With Closing Costs

Purchase price: $188,900

Property type: New construction, single-family home

Down payment (20%): $37,780

Loan type: 30-year fixed DSCR

Interest rate / APR: 7.125% / 7.508%

Seller concessions: $2,500

Total cash to close: $45,713

(Down payment plus lender fees and closing costs after concessions)

Loan amount: $151,120

Monthly Ownership Costs

| Expense | Monthly |

|---|---|

| Principal & Interest | $1,018.12 |

| Property Taxes | $157.42 |

| Insurance | $115 |

| HOA | $50 |

| Subtotal (before management) | $1,340.54 |

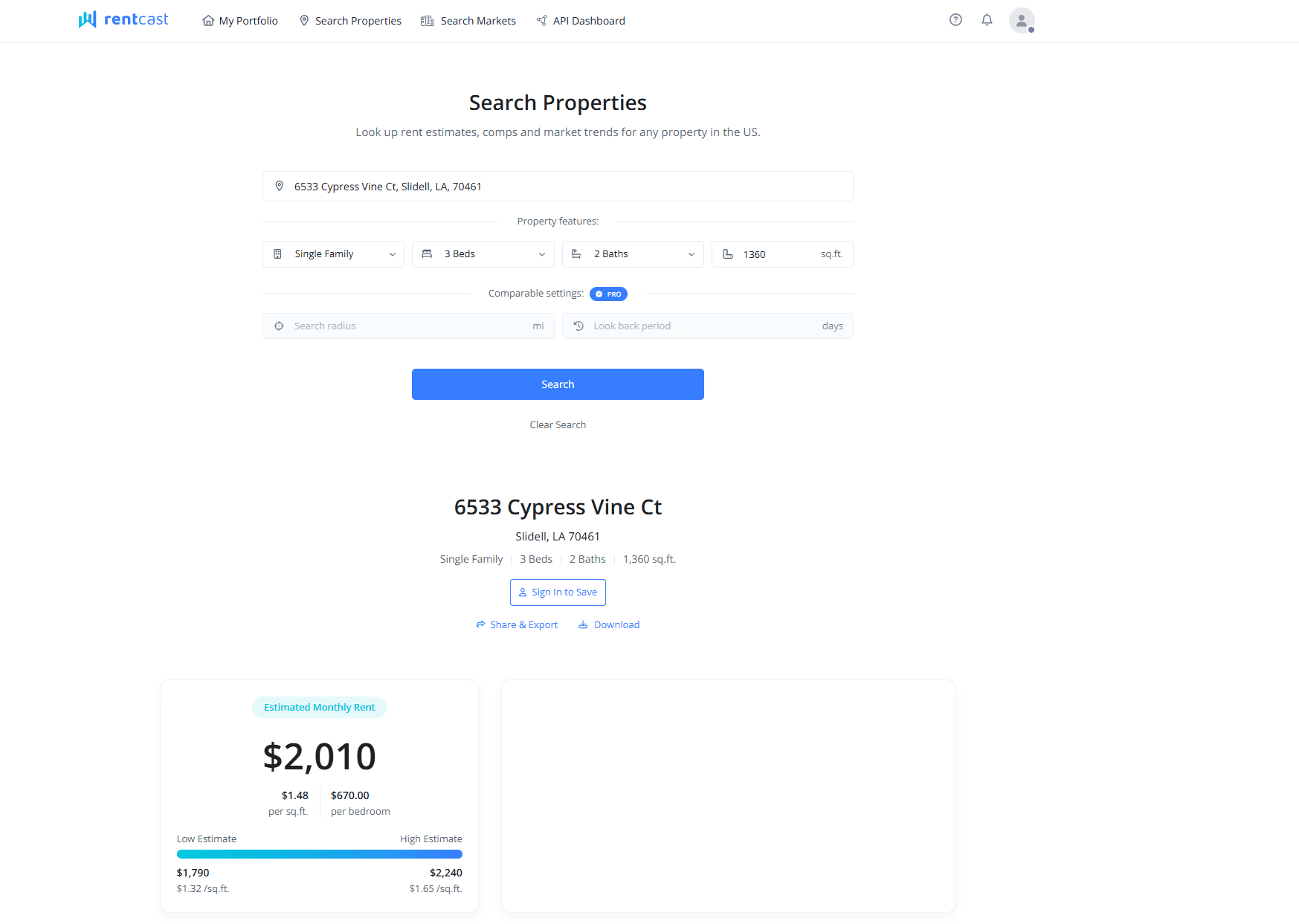

This Is A Screenshot From A Website Called Rentcast Which Will Give You A General Idea Of What A Home Will Rent For Based Upon The Street Address Given

Conservative Rental Income Assumptions

This model assumes slow, steady rent growth, not aggressive projections.

| Year | Monthly Rent |

|---|---|

| Year 1 | $1,950 |

| Year 2 | $1,975 |

| Year 3 | $2,000 |

| Year 4 | $2,025 |

| Year 5 | $2,050 |

Property Management

(The Real Cost of Being Hands-Off)

This investor chooses professional property management.

Management fee: 10% of collected rent

| Year | Annual Management Cost |

|---|---|

| Year 1 | $2,340 |

| Year 2 | $2,370 |

| Year 3 | $2,400 |

| Year 4 | $2,430 |

| Year 5 | $2,460 |

Updated Monthly Expenses (Year 1)

Base ownership costs: $1,340.54

Property management: $195

👉 Total monthly expense:$1,535.54

Net Monthly Cash Flow (Year 1)

Rent: $1,950

Expenses (including management): $1,535.54

👉 Net cash flow:$414.46 per month

This cash flow is not spent.

How the Cash Flow Is Used

Rather than increasing lifestyle expenses, the investor allocates cash flow conservatively and this is done to be used in case any repairs need to be made on the rental property. Since this is a new home, the builder should issue a 1 year warranty.

Monthly Allocation

$300/month → High-Yield Savings Account (3% Interest Gain)

$114.46/month → Stock market investment (8% Interest Gain)

This approach:

Builds a true emergency fund

Adds diversification outside real estate

Maintains liquidity

Keeps the model conservative and repeatable

This is for informational purposes only and not tax advice. Everyone's situation is unique. Seek advice from your own tax professional concerning your unique situation.

Investor Profile (Tax Context)

Age: 45

Filing status: Single

W-2 income: $100,000/year

Federal marginal tax bracket: ~24%

State taxes: Not included (varies by state)

Why Taxes Don’t Destroy This Deal

Rental income is not taxed like W-2 income.

Deductible Expenses Include:

Mortgage interest

Property taxes

Insurance

HOA dues

Property management fees

Depreciation

Depreciation (Estimated)

Depreciable value: ~$151,120

Annual depreciation: ≈ $5,495

Result (Simplified)

After deductions and depreciation, the rental income is close to tax-neutral, even though it produces positive cash flow.

This is one reason high-income earners often use real estate as a long-term wealth and tax-efficiency tool.

(Always consult a tax professional.)

Property Growth & Equity After 5 Years

Annual appreciation: 2.125%

Estimated value after 5 years: ≈ $210,300

Remaining loan balance: ≈ $141,000

👉 Equity after 5 years:≈ $69,300

Investment Account Growth (5 Years)

📈 Stock Market Portfolio

Initial investment: $114.46

Monthly contribution: $114.46

Assumed return: 8% annually

Total contributions: ≈ $6,982

Estimated value after 5 years:≈ $8,500

🏦 High-Yield Savings Account

Monthly contribution: $300

Interest rate: 3%

Estimated value after 5 years:≈ $19,500

This is fully liquid capital.

Total Net Worth After 5 Years

| Asset | Value |

|---|---|

| Home Equity | ≈ $69,300 |

| Stock Portfolio | ≈ $8,500 |

| Emergency Savings | ≈ $19,500 |

| Total Net Worth | ≈ $97,300 |

What This Scenario Actually Shows

This investor:

Bought one modest new construction rental

Used professional property management

Took zero shortcuts

Made conservative assumptions

Invested only the remaining cash flow

Never relied on appreciation alone

And still built nearly $100,000 in net worth in five years — while maintaining a full-time W-2 income.

Final Thought

This is what boring, disciplined investing looks like.

Not flashy.

Not viral.

But repeatable.

Wealth isn’t built by chasing perfect deals — it’s built by executing solid ones consistently.

Important Disclaimer

This example is for educational purposes only. Returns, tax outcomes, and expenses vary by individual situation. Always consult your CPA, tax advisor, or financial professional.

Purchase a Home

Whether you're buying your first home or your dream home, we have a mortgage solution for you. Get your custom rate quote today.

Refinance your Home

We're committed to helping you refinance with the lowest rates and fees in the industry today. Getting started is quick and easy.

Apply Today

Our secure application is a few quick questions that takes about 7-10 minutes to complete and is required for a “Pre-Approval”. Get started today!