A Tale of Two Brothers: Renting vs. Buying Over 30 Years

What happens when two people do nearly everything right financially—but make one different housing decision?This simplified hypothetical explores how time, discipline, housing costs, and appreciation affect long-term net worth. The numbers are intentionally clean and conservative, but the lesson is anything but small.

The Starting Point

Two brothers:

Same age

Similar income

Same neighborhood

Same $30,000 saved

Both financially disciplined

The only difference?

One buys a home. The other rents and invests more aggressively.

Brother One: The Homeowner

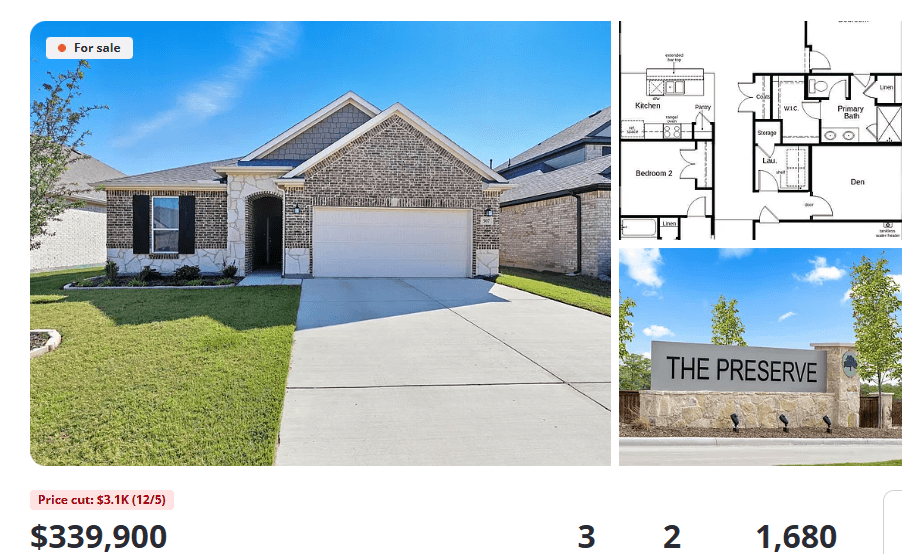

Brother One purchases a 3-bedroom, 2-bath home, approximately 1,700 square feet, listed for $339,900 after it’s been on the market for about three months.

That time on market gives his real estate agent leverage, and they successfully negotiate $5,000 in seller concessions toward closing costs.

Loan & Purchase Details

Loan type: FHA 30-year fixed

Credit score: 620

Interest rate: 5.75%

APR: 6.60%

Down payment: 3.5%

Monthly Housing Costs

Principal & Interest: $1,947.64

Property taxes: $380

Homeowners insurance: $300

HOA: $60

Total monthly payment:$2,837.10

Cash Position

Total out-of-pocket: $19,399

Remaining cash: ~$10,600

He invests:

$5,000 into a Roth IRA

$25 per month thereafter

Assumes an 8% long-term return

Brother Two: The Renter-Investor

Brother Two values flexibility.

He rents a comparable home in the same neighborhood for $2,100 per month.

Instead of buying, he invests:

$25,000 upfront

$400 per month

Assumes a 9% return

Every five years, he renews or relocates, with rent increasing by $100 per month each time.

After 5 Years

Brother One (Buy) Brother Two (Rent + Invest)

Total Spent (5 yrs)$196,125 $175,000

Net Worth (5 yrs)

$93,735

$69,312

Monthly housing cost at Year 5$2,837 $2,100

| Brother One (Buy) | Brother Two (Rent + Invest) | |

|---|---|---|

Total Spent (5 yrs) | $196,125 | $175,000 |

Net Worth (5 yrs) | $93,735 | $69,312 |

Monthly housing cost at Year 5 | $2,837 | $2,100 |

Difference in spending: $196,125 − $175,000 = $21,125 more spent by Brother One

Thirty Years Later: The Long-Term Impact

Brother One at Year 30 (3% Appreciation)

With 3% annual appreciation, the home’s value grows substantially over time.

Home value: ~$825,000

Mortgage balance: $0 (paid off)

Roth IRA: ~$45,000

Total net worth:~$870,000

Total spent over 30 years:~$1.05 million

At this point, Brother One lives mortgage-free, with only taxes, insurance, and maintenance to manage.

Brother Two at Year 30

Monthly rent: $2,600

Investment portfolio: ~$795,000

Total net worth:~$795,000

Total spent over 30 years:~$1.02 million

Despite investing diligently for decades, Brother Two has no housing asset and must continue paying rising rent.

Years 31–32: Where the Paths Truly Separate

Once the mortgage is gone, Brother One redirects cash flow.

New Strategy

Maxes out his Roth IRA

Invests the remaining surplus into a taxable investment account

Total new investing: $1,500 per month

Assumes an 8% return

At Year 32

Home value (continued 3% growth): ~$875,000

Roth IRA: ~$66,500

Taxable investments: ~$24,000

Total net worth:~$965,500

Brother Two at Year 32

Rent: $2,700 per month

Investment portfolio: ~$820,000

Brother Two still has a strong net worth—but his housing cost never disappears.

What This Scenario Actually Shows

This story isn’t about declaring a winner.

It shows how small differences compound massively over time.

Key takeaways:

Renting can work — but it requires perfect discipline for decades

Homeownership benefits from leverage + appreciation

The biggest wealth acceleration happens after the mortgage is paid off

Rising rent becomes a permanent drag on cash flow

At 3% appreciation, homeownership isn’t just competitive — it becomes a wealth accelerator.

Important Advantages of Homeownership Not Fully Quantified

This hypothetical intentionally stayed conservative. It did not include:

Refinancing opportunities at lower interest rates

Tax advantages of homeownership

Capital gains exclusions on primary residences

Housing stability and freedom from forced moves

Protection from long-term rent inflation

It’s also highly unlikely someone rents the same home for 30 years without disruption.

Important Disclaimer

This scenario is a simplified hypothetical for educational purposes only.

Real life is far messier:

Interest rates change

Refinancing may or may not be available

Property taxes and insurance almost certainly increase

Market downturns were not modeled

Brother Two would need to remain perfectly disciplined for decades

Life events—job changes, family needs, health issues—can interrupt even the best plans

These numbers are not predictions or financial advice, but illustrations of how different choices behave over long periods of time.

Final Thought

The real question isn’t:

“Should I rent or buy?”

It’s:

“Which decision gives me the most control when life inevitably changes?”

For some, that’s flexibility.

For others, it’s stability.

But when appreciation, leverage, and time work together, the math quietly shifts—and staying on the sidelines can become the more expensive choice.

Purchase a Home

Whether you're buying your first home or your dream home, we have a mortgage solution for you. Get your custom rate quote today.

Refinance your Home

We're committed to helping you refinance with the lowest rates and fees in the industry today. Getting started is quick and easy.

Apply Today

Our secure application is a few quick questions that takes about 7-10 minutes to complete and is required for a “Pre-Approval”. Get started today!